There are days where decades happen…

Over the weekend, a performative, slow-motion drone swarm in the Middle East mercifully caused little real world carnage. The real collateral damage was to the prices of cryptocurrency tokens (excluding resilient memecoins).

Other than our beleaguered $CRV token, most token prices would swiftly recover. For fans of Curve, we’ll content ourselves with a successful display of Curve’s robust fundamentals, which will be nice if fundamentals ever matter in crypto.

For several weeks the absurd demand for leveraging long Bitcoin/Ethereum had been driving up interest rates right up to the edge of dragging down the $crvUSD peg. In the course of a weekend, balance was restored.

The dramatics also marked a successful stress test of the Llama Lend protocol. The isolated lending markets all performed quite strongly throughout the proceedings.

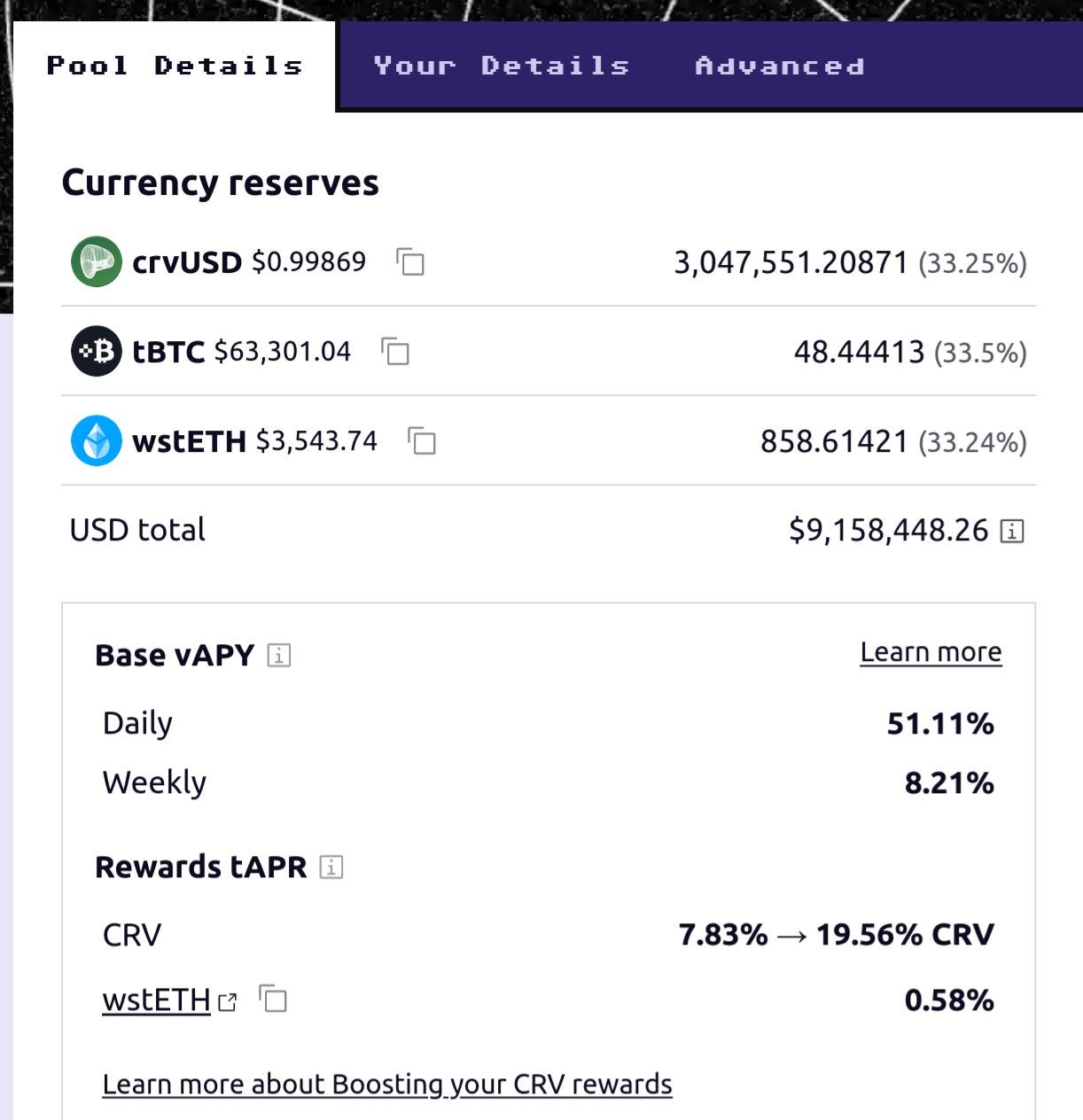

Just before the shenanigans from the weekend, there was more fascinating activity occurring on the Llama Lend markets on Arbitrum.

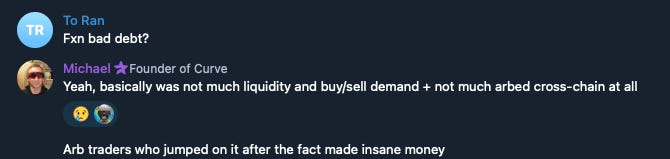

Most of the highly markets heavily traded by arbitrage traders fared very well. However, on the nascent Arbitrum market for $FXN, there was essentially no cross-chain arbitrage traders, so the price of the token on the L2 was wildly different from the price on L1.

While this presented a highly profitable trading opportunity for the people who picked up the trade, it also caused a small amount of “bad debt” for suppliers on the market.

The situation regarding the $FXN market is a great illustration of the risks lenders may face in Llama Lend. The lending APY alone is often good enough incentive for suppliers, and occasional rewards atop this make it great. But lenders should not blindly ape, but consider factors like available onchain liquidity and whether the markets are well arbitraged.

If things explode, suppliers may find themselves with their hand caught in the cookie jar. If you have considered these risk and are still unconcerned, note that the lender APY for the $CRV markets on mainnet was incredibly tantalizing after this past weekend.

One final note on the Llama Lend supply side. In a bit of a highbrow retort to critics, Mich deployed a rather novel 3pool called “Real World Mansion USD,” for CRV-crvUSD lending market deposits in Llama Lend, Silo Finance, and UwU Lend.

The pool’s jumped to a couple million in TVL, seems as though mansions are popular. Is this part of Mich’s plan to repay his debt while educating the masses about lending markets along the way?

Elsewhere around Curve’s classic DEX business, the pyrotechnics left a lot of onchain rubble investigators are still sifting through. For instance, what caused so much trading activity through wstETH…

And the mystery of what’s going on with stETH lately…

It all appears as if we’ll enjoy another banger of a week in terms of fees. Curve’s been generating a million in revenue each week since late April, and the first half of this week it looks as if trading fees are already ahead of recent weeks.

Help us by sharing this post on 𝕏