April 20, 2022: Flywheel-nomics 101 🎡♻️

April 20, 2022: Flywheel-nomics 101 🎡♻️

State of the Flywheel as Convex passes 200MM $CRV

Congratulations to Convex on passing the 200MM $CRV marker!

Wut means? It means if you’re asking “Wut Means,” then pursue higher education.

The short version is that $CVX emissions are pegged to how much $CRV the protocol has farmed. We’re currently sitting at 88.6% of all CVX that will ever be released. The supply of $CVX being released tapers off sharply from here. According to Economics 101, less supply is good for price if demand persists.

@DefiDividends’ great website tracks whether or not $CVX is inflationary at https://daocvx.com/supply/ - lately this has been converging.

Big thanks to the anons who made it all possible, not just for dreaming up brilliant tokenomics from the outset, but for their relentless execution throughout! They could have rugged the project for billions of dollars, but apparently see greater value in building Convex long-term.

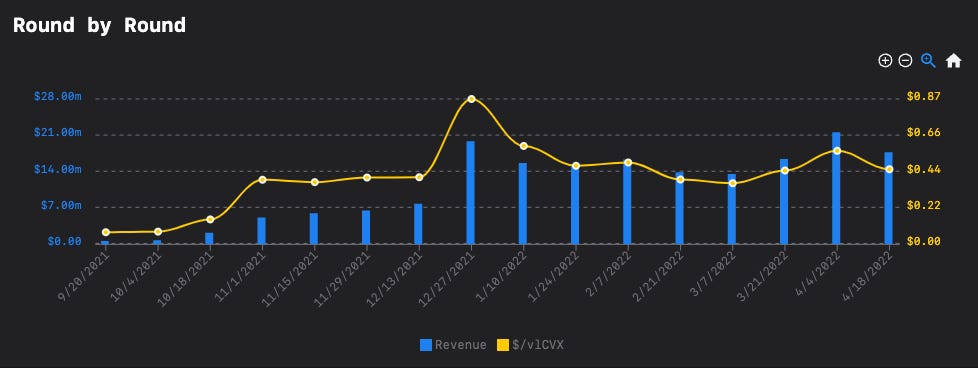

Not to be outdone, the industrious FUD merchants are also keeping busy, now complaining about the drop in the recent Votium round, and bribe efficiency dipping below $1 on the dollar.

The most recent Votium round is well-covered in this thread and the detailed projections of @WAGMIAlexander, featured on Kingmaker’s twice monthly Bribecast.

The giga-brained challenge with covering $CVX relative to its bribing efficiency is the flywheel effects. We’ll try to review these dynamics as best we can, but recursion makes our head spin.

Protocols who want to bootstrap liquidity have a few different choices, most notably:

Directly buying $CRV for veCRV

Directly buying $CVX for vlCVX

Submitting bribes to Votium to influence others’ vlCVX

Hope and prayer

For the first several rounds, bribing through Votium bribes were unquestionably effective. Llama Airforce tracks this as the Emissions / $1 spent on bribes metric, which historically tended to return more than $1 for every dollar spent.

Efficient markets abhor such free arbitrage, so more recently we’re seeing Ms. Market converging below parity.

Suddenly the other options are becoming more competitive. Option 2, buying $CVX, has been quite attractive for much of the past year among forward-thinking protocols who were able to plan a few moves ahead. Some lucky duckies bought $CVX in the $2 range. Lately it’s cost about 10x that.

With options 2 and 3 getting saturated, the choice of last resort is the most distasteful… what about $CRV? Ew, gross! $CRV requires locking and constant relocking! And all those crypto-Twitter “influencers” said $CRV was the worst tokenomics in the world! Until everybody eventually embraced it, that is.

Oh well. Desperate times call for desperate measures. As $CVX gets pricy, attention shifts back to veCRV.

$CRV is quite abundant relative to $CVX. Even if it’s more of a hassle to deal with $CRV, if the price is right then protocols will at some point embrace the discount. Accordingly, we’re starting to see interest in directly bribing veCRV holders heat back up. A new dashboard for the veCRV market makes this clear:

Hypothetically, if demand for $CRV increases and its price also goes up, things get messy. What does a rising price of $CRV do for a protocol, particularly for the protocol that controls a massive swath of veCRV? 🤔🤔🤔

And thus extremely smart people get stuck weighing which particular gear in the flywheel is more valuable. Is it $CRV or $CVX that makes the carousel go round?

The intricate dynamics of flywheel economics could make anybody’s head spin. We don’t pretend to fully comprehend it ourselves. We instead prefer sitting back and simply enjoying the ride (not recreational advice).

Of course, understanding the mechanics of how a flywheel operates is one thing. The portion we didn’t cover yet is the state of the demand side — the whole flywheel might fall apart if nobody wants to use it. Tomorrow we’ll review the state of the demand side…