August 23, 2022: A $DOLA Short 🚩💸

August 23, 2022: A $DOLA Short 🚩💸

Crypto Risks Team Recommends Against Raising Pool’s "A" Parameter

The Crypto Risks Team has spoken!

As we’ve learned in previous incidents, the existence of the Crypto Risks team is vital to keeping the Curve ecosystem safe. Absent voices of precaution, the Curve DAO might simply YOLO approve anybody or anything asking for a gauge.

Yet some protocols may be poorly designed, or outright fraudulent. Back when the market was bullishly raging upwards, new protocols were popping up faster than anybody could research them. The Curve community approved a community grant to fund the Crypto Risks Team, essentially a think tank dedicated to researching new protocols and evaluating their risks.

They’ve become a crucial check and balance within the system. If we can’t or won’t successfully self-police, we have no claim to building a superior financial system.

Therefore, when the team advises we pump the brakes on a governance proposal, we’re best off listening. They’ve done exactly this by sounding the alarm on the $DOLA proposal to raise the A parameter on the $DOLA pool which we highlighted last week.

Fortunately for all, Inverse Finance clearly doesn’t fall into the “scam” category. By all indications, they’re a thoroughly honest team who have suffered from particularly bad luck in the form of sophisticated hacks but are working hard to rebuild.

The hackers in this case were deviously brilliant. The above Rekt articles provide a great summary of the grisly incidents, in which a price oracle was manipulated using sophisticated MEV techniques and loads of money.

As twisted as these attacks were, nobody in the community was stupid enough to call to censor Tornado Cash, which was used in the getaway. Such a ridiculous move would only backfire to expose whoever issued the request to be an imbecile, so it’s good our extended crypto family is a bit more shrewd.

Sadly, this looks to be yet another of several cases where medium sized players in DeFi have a rougher time than larger players. This particular attack required enough funds to manipulate the price of $INV used to borrow assets — with 64MM $DOLA in existence, the attack was more affordable for the bad guys. A total supply in the billions may have cost too much to manipulate prices in this manner.

Inverse Finance hit a spell of bad luck in this case. At the time of the attack, Rekt reported the protocol was saddled with $10.63MM worth of bad debt and just $20MM TVL. That’s a tough climb, but to their great credit they’ve continued working to build their way back. It contrasts favorably with how other protocols have lately closed up shop by funneling user funds to bail out investors.

A few months later, Inverse has approached the Curve DAO seeking to raise the A parameter.

Today the protocol is continuing to work their way out of debt — the total bad debt at the moment is $15.79MM via Risk DAO.

In the governance forum, @cryptoharry notes that this combines the debt from the hack (~$10MM) along with other debt on the protocol. It’s a large figure. In the governance proposal, @cryptoharry lays out the plan to make good on this debt.

The bond stats page linked at the end provides a window into the status of these bonds.

Most recently the bulk of this is coming from $DOLA bonds, $188K in July. It’s certainly a good effort, but a ways from making a serious dent. If you want to jump in yourself, the rates are all over the place at the moment.

Much of the conversation in the governance proposal comes down to the question of who absorbs the risk. Quoth @chanhosuh

“There is no free lunch. Someone has to bear the cost for the benefits going to traders. The cost is carried as risk by LPs.”

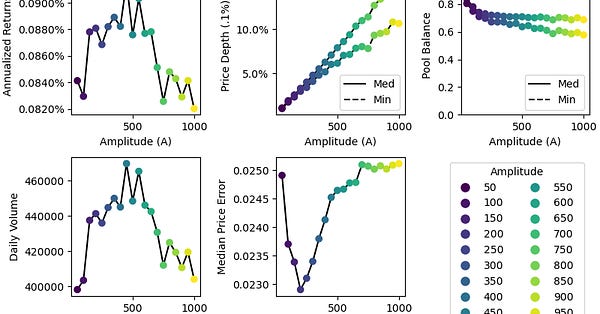

What particularly raised red flags among the risks team was an indication that $DOLA was relying on the Curve pool to protect the beleaguered stablecoin’s peg. As we saw in the collapse of UST, a v1 Curve pool cannot protect a peg in and of itself. The Stableswap Invariant can only protect a peg when the underlying fundamentals actually imply such a peg exists in the first place. Even mighty Egorov’s boldest math could not peg a Euro note to a dollar bill.

Running through some stats here — there’s a total of 64MM $DOLA in existence. The bulk of this, 52MM, sits in the Curve pool.

Along with the 3pool tokens, this is ~$93MM earning Curve rewards. 99.9% of this is staked on Convex, so we can easily see how much this is earning through the aspirational dashboard of Convex yield farming stats.

Staking this is currently yielding ~25K per day worth of $CRV rewards. If this full amount went to repaying the debt and nothing else changed, then the protocol could make $10MM in about 400 days. Of course, it doesn’t work exactly like this, but it helps to give an indication of the size of the hole we’re crawling out of.

Would this be a viable plan even if this entire balance was accrued to Inverse? According to Inverse Finance pre-hack, probably not:

In truth, the Inverse Team is lucky they have a gauge in the first place. Their pool was created a year ago, before the Crypto Risk Team was capable to provide such scrutiny for new gauges. Given the team has not conducted any audits, this fact would probably raise red flags by the Crypto Risk Team if the protocol were applying for a gauge today.

Luckily for the team they appear to be grandfathered into a gauge, unless the DAO gets aggressive. Ergo, their LPs are soaking up about $25K/day worth of Curve.

One such LP is Concave Finance, which boasts an “a sizable eight digit position in the DOLA+3CRV pool.” This gives Concave a >10% influence over the pool.

In their post, Concave claims:

“We are aware of larger wallets that are potentially interested in this Pool, and we believe an increase would be mutually beneficial since there would be less slippage from entering or exiting larger positions”

We couldn’t possibly evaluate whether or not this claim is true. However, we presume these whales are interested in depositing 3CRV tokens, since there’s not enough $DOLA supply presently in existence for wallets with an order of magnitude more $DOLA than Concave’s 8 figures to exist (unless these rumored whales are planning to mint new $DOLA.)

Perhaps a good next step would be for these whales to chat directly about their plans with members of the Crypto Risk team, who could better evaluate if an increased A parameter is the best strategy to achieve these goals.

At one point it appeared there could be interest in creating an INV-DOLA Curve v2 pool, but this never appears to have gotten off the ground. It would be interesting to hear from the team their thoughts on how this could have fit into their architecture.

We’re pleased to see Inverse Finance is working hard to recover from these unfortunate events, and we’re just as pleased to see the Crypto Risk team is working overtime to ensure this is done in a safe manner that protects LPs. We’re certain that all these big brains colliding can create a great solution for everybody.