August 25, 2022: $cbETH 🏦🥩

August 25, 2022: $cbETH 🏦🥩

Coinbase ETH Joins the staked Ethereum wars

The merge is a month away, but the fun is already starting. Yesterday Coinbase stepped up the high-stakes Ether staking game.

Coinbase as a company requires no introduction, but their role in the upcoming merge deserves more attention. When we’ve looked at the staking game in the past, we’ve mostly been focused on Lido and RocketPool, but this is just a narrow slice.

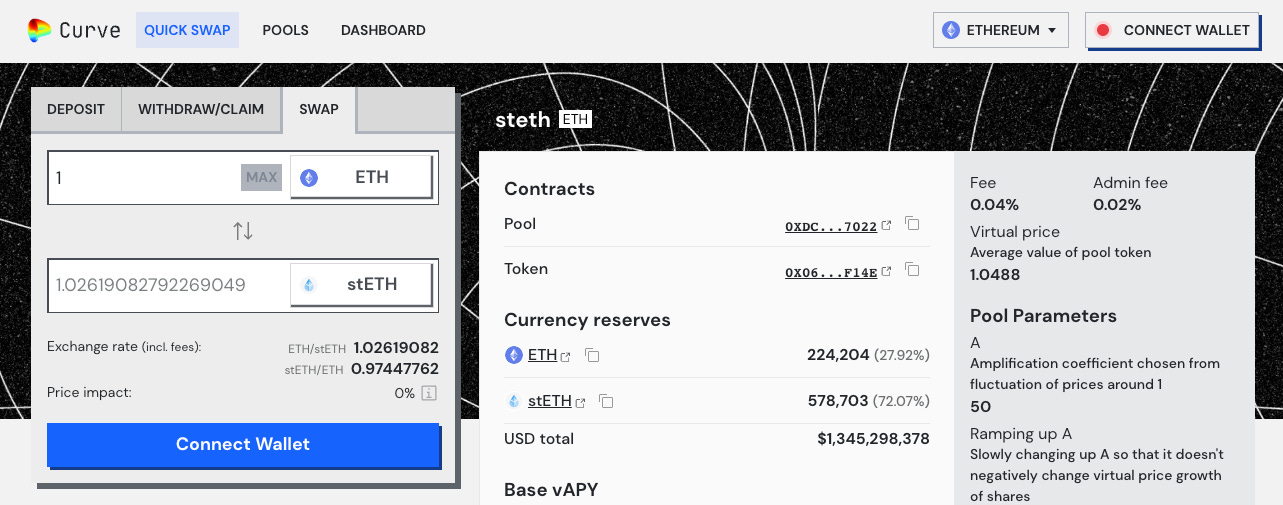

The actual breakdown of ETH stakers has been historically quite diffuse — initially the game was dominated by whales and centralized exchanges, but more recently liquid staking options started to grab market share. The details are all laid out in a great series of Dune dashboards by @hildobby.

We see a lot of players staking eTH. Although Lido controls most of the liquid staking market, the CEX portion is presently dominated by Coinbase.

Coinbase staking is a big business — representing 8.5% of the company’s revenue. This dashboard suggests almost 2MM ETH staked by Coinbase — the $cbETH smart contract lists a total supply of ~650K, about a third this total.

For a centralized company, this represents a surprisingly daring move. Crypto hostile regulators in the US have singled out Coinbase perhaps more than any other company. As Owen Fernau fished out from filings, the government’s DDOS-by-subpoena hack has taken direct aim at Coinbase’s staking operations.

For a company that works hard to stay at the forefront of compliance, it would have been far easier to stay out of the staking game altogether. Yet they appear to be digging in their heels with under a month to go until the merge.

In the run-up to the merge, there’s been a lot of concern about centralization of validator power within the US, including Coinbase’s position as the second largest set of validators. In discussing the hypothetical event of Coinbase being compelled to implement damaging protocol-level censorship, the company has declared its preference to forego staking altogether.

There’s a plausible chance the second largest validator could be forced to go dark during the merge. You’re advised to keep your popcorn stashes at the ready in the upcoming month (neither financial nor nutritional advice).

The white paper released yesterday is a good read, and we’ll direct you to the following good analyses:

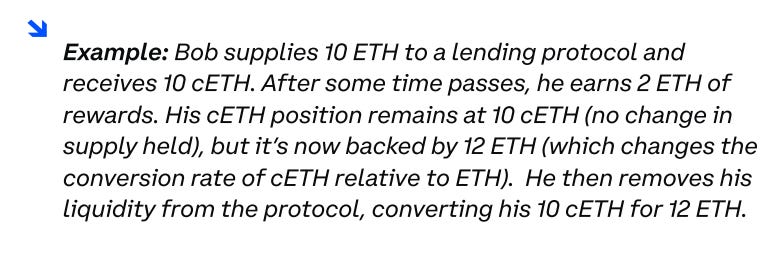

Of particular note is their section on DeFi applications. Yesterday a cbETH:ETH Curve pool appeared out of the blue, with ~1K ETH in funding.

This is fairly exciting news for Curve in several ways. We know that Lido’s much larger stETH:ETH Curve pool has been instrumental in its long-term staking journey. For the longest time the pool held the two tokens at parity, until the run-up to the merge pushed this to a small imbalance.

As interesting as it’s been to watch this play out, the Coinbase pool is launched as a Curve v2 pool. This was a good choice, given that $cbETH operates under a cTokens model as they describe in the white paper.

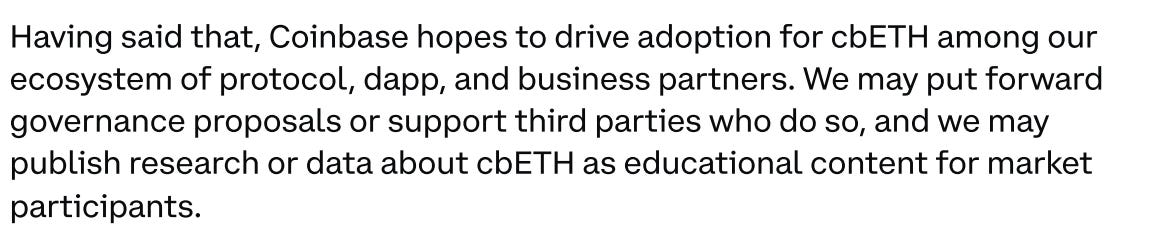

As Coinbase earns staking rewards, the value of a $cbETH ticks upwards incrementally. The idea is that a $cbETH purchased for 1 ether today could get back more ether tomorrow if all goes well. Redemptions is apparently not yet live.

Then again, the existence of the Curve v2 pool means trading is effectively open for business. A Curve v2 pool is in many ways just as good.Just as has happened with other v2 pools, this pool may become the best window into how the market is valuing $cbETH in realtime.

Interestingly, a $cbETH is trading under 1 ether at the moment. Is there real concern among traders that a $cbETH may not be fungible in the future, or is this a temporary imbalance traders could use to profit off the merge?

For Curve users hoping that Coinbase is likely to jump into the birbs game, I’d guess this is unlikely. In their white paper they outlined the scope of their involvement, and it sounds somewhat hands off.

One imagines with regulators breathing down their neck they’d be unlikely to push too heavily in this direction. Besides, it’s probably not necessary. Curve v2 pools have proven historically to be unstoppably accurate even without incentives.

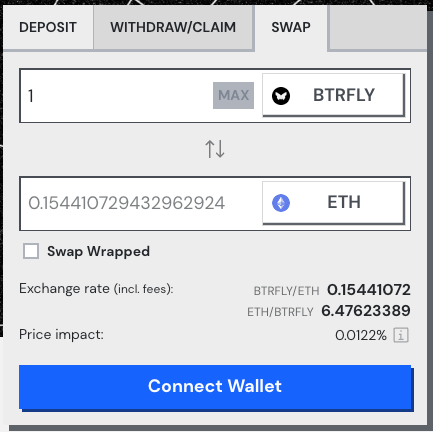

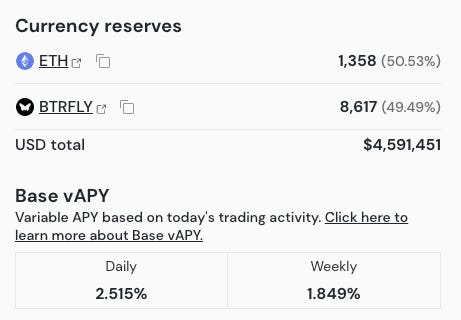

By way of example, the $BTRFLY / ETH pool has been keeping up just fine with rapid price movements on $4.5MM in liquidity, earning LPs good trading fees (albeit with risk of loss due to prices movements).

There’s two pools $cbETH pools deployed to Curve, but one of which is empty. Always be careful to make sure you’re using the correct pool.

An easy way to check that the coin you’re looking at is actually $cbETH: look at the blacklist function. If it’s running on overdrive, it might be operated by Coinbase.

It is what it is — acting as the AOL of DeFi has certain obligations. If we want to have a service easy enough for boomers to use, it’s going to need to comply with insatiable appetite for censorship from regulators.

FWIW, Coinbase’s USDC has technically banned fewer addresses than its rival Tether.

Although, this may be in part due to Tether taking more aggressive actions in response to hackers.

Tether is earning some plaudits from the crypto community for taking a more principled stand in response to OFAC sanctions. While it’s likely Tether will just wait until they receive a direct request from law enforcement before also falling in line, it’s a refreshing difference in tone compared with other companies who raced to see who could slam their knees into the ground fastest.

The aggressive posturing of governments towards cryptocurrency remains the biggest active threat towards our community. Cryptocurrency as a technology will of course be fine no matter what governments try to do, but the assault on speech and privacy rights directly assaults the freedoms of everybody who lives in supposedly free countries.

We’re expecting tomorrow’s newsletter to review this topic in more detail as well, but the issue is too important to delay so here’s some resources for those who want to take action today: