February 21, 2024: Ethena's War Cry 🛡️🦉

$USDe launch sees $287MM minted in fight for 27% in hedging yields

Help us by sharing this thread on 𝕏

Wake up, babe… a new stablecoin shelling out >20% APY just dropped!

Luna PTSD? Is our fledgling bull run about to collapse at an even more accelerated pace?

Calm down! While the long-term viability of their model requires time to be proven out, Ethena is certainly far from the nightmarishly endogenous Ponzinomics that cut short our last bull. Given that $300MM has flowed into their platform in the past few weeks, it appears the community has also chosen to vote with their dollars.

Naturally, a higher than market rate APY will always set off red flags at the same time it pulls in degens. The question usually works out to whether this is elevated because you’re early, or whether it’s because the market is pricing in a higher risk? Let’s walk through these yield mechanics.

Coindesk, which described the mechanics via its headline as “Earning Yield by Shorting Ether,” elaborates more in the article:

There’s now plenty of other good background reading we recommend to review the mechanics.

The Ethena docs go into very good detail:

Putting aside the stETH yield, which we consider a fairly known quantity at this point, let’s just consider the funding rate side. History shows that the “27% yield” the token is generating at present is mostly because of the present greed in the Ethereum markets at the moment, and over the years this number been more sedate.

While this earned rate is variable, in 2021 it yielded ~18%, in 2022 ~-0.6%, and in 2023 ~7% APY on a volume-weighted basis.

In all, the Ethena team have put together a lot of good and interesting material, all of which is certainly worth your time to read. In addition to their Gitbook docs, another recommended read is their Mirror post boiling this all down to the concept of an Internet Bond

Fancy words and theories are nice, but the important question is whether it will work?

As is so often the case in crypto, the strategy has been tried before. That’s not always a knock against the strategy… so many things that failed in the past have gone on to succeed now that crypto has more users. The question is more why it failed, and if they’ve learned from the lessons.

The prior attempts got felled during the lean times. How do the protocols survive when funding rates turn negative? Their head of research Conor Ryder posted a lengthy post, boasting “USDe has been built with negative funding in mind”

The post describes that periods of negative funding rates are usually short-lived. He lays out expectations for how the protocol would operate in leaner times, and describes the existence of an insurance fund to cover such days.

Our microbrain first take on all this is that negative funding may not be the only lean times they’d face. In less exuberant times, if their yields stay positive but below DeFi yields (or even treasury yields), how loyal will capital prove?

Nagaking, one of the Curve gigabrains, offered his far smarter take (reposted with permission):

Definitely less risky than Terra, but still lots of ways to blow up. Their risk analyses are a bit naive: they rely on historical funding values but don’t think enough about how their product will distort those if it gets big enough

Maybe we can just hand wave it away for now… get the money first, then if times turn lean you can figure out your next pivot. Speculative frenzies don’t last forever, what blessed timing for their launch…

Whatever may happen in the future, at least in the immediate present we’re satisfied that it’s not a house of cards in imminent danger of collapse.

You may (or may not) take some comfort from their backers, which boasts some heavy hitters…

We haven’t seen confirmation from Mich about his involvement, nor have we seen any denial.

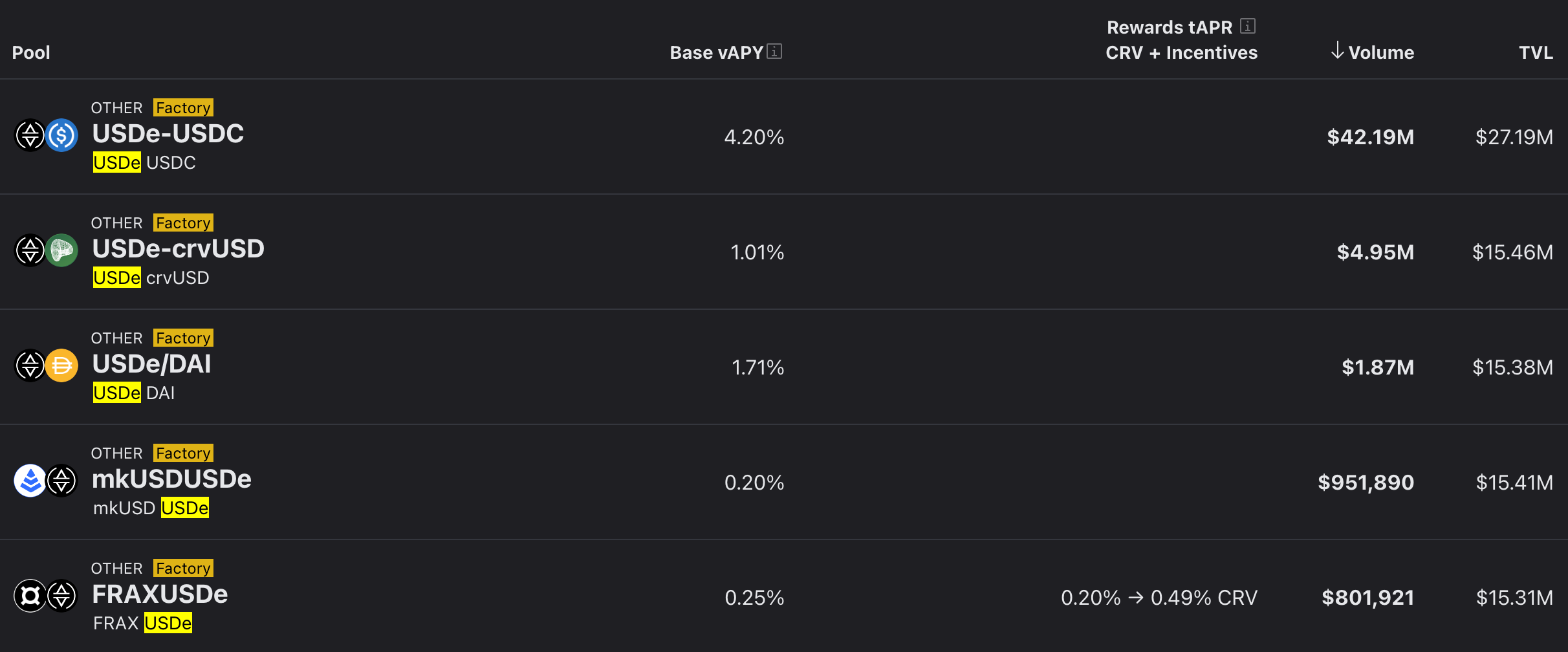

If he is involved, perhaps it might explain why the team chose to set up liquidity pools on Curve, where heavy volume of $USDe has been spotted.

Lookit those utilization numbers…

But… why?

In this case, it’s due to the first epoch of Ethena’s “Shard Campaign” which is tracking deposits to the Curve pool.

A shard campaign, their blog explains, stemmed from blowback against “points” campaigns. Shards are distinct…

The “difference” is the short term nature of the campaigns, the first epoch is for LPs into Curve. They offer a video walkthrough here:

So… even if you don’t plan to ape, the fact other users are busy aping on Curve can work to your benefit. The nice thing about Curve is that this even works to your benefit if the underlying protocol collapses.

The extreme case of Luna was in most ways good for Curve. It brought lots of volume while UST was active, which got burnt into 3CRV and distributed to veCRV holders, no need to touch UST. Or to go back to Nagaking again:

Advantage of veCRV that doesn’t get enough attention: you get a slice of that yield without owning the risky asset

Although, as Alunara retorted… (also posted with permission)

Fun fact: Luna (LUNC) market cap is still higher than CRV market cap

So maybe it was Curve, not Luna, that was the risky part of the equation?