June 20, 2023: Post the W 📣🎉

Curve DAO votes to onboard wBTC and WETH as $crvUSD Collateral

The Curve ecosystem is becoming so active, it threatens to flippen itself with each new week of governance votes.

We’re preparing a pair of posts covering all the recent governance action. Today we cover all the latest votes affecting $crvUSD, tomorrow the remainder…

crvUSD

Collateral Types

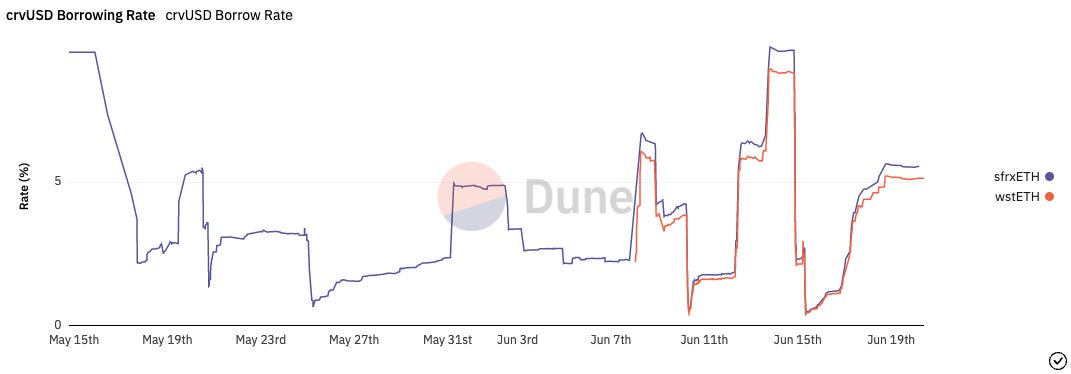

By now we’re quite accustomed to observing the total market cap of $crvUSD seesaw between rapid growth and plateaus, in response to the ebb and flow of borrowing rates.

In other words, it’s working as designed. The dynamic borrowing rate is a tool intended to adjust automatically to control supply/demand for the stablecoin and reinforce its peg. With rates sitting around 5% the past few days, does that mean there’s no growth catalyst for the upstart token? Cue the death spiral000rs…

There’s some hopium on the horizon. In the next week or so, the $crvUSD collateral markets will likely be diversified even further. We can’t be sure what effects this will have, but let’s guess. Our expectation (not financial advice) is that a quick surge of users in the new markets will cause borrow rate to rise even further. Always be wary if you’re playing the latest reindeer games.

wBTC

The new collateral type we’re watching most closely is the potential addition of wBTC.

In a governance forum post, Mich ran some simulations you can easily replicate to demonstrate how the addition of the new collateral might play out.

As the first non-Ethereum collateral type, it has significant potential to reshape $crvUSD. A lot of wrapped Bitcoin has found its way onto Ethereum in search of yield. At present, nearly 1% of the total Bitcoin supply now has been wrapped onto Ethereum, which makes wBTC the 17th largest token on CoinGecko.

However, in our protracted bear market, this massive pool of wealth has been largely underutilized. The going market rate for wrapped Bitcoin in Ethereum DeFi is yields in the low single digits.

It may be enticing for $wBTC holders who don’t want to sell a single sat to simply hand their Bitcoin over to the safekeeping of Mich’s magical math, then use $crvUSD to chase higher dollarcoin yields. It’s absolutely our pick for the most interesting new market to keep an eye on going forward.

WETH

The addition of WETH as collateral has also been in high demand, particularly among decentralization advocates who have concerns about potential centralization of ETH LSDs. In chats, Mich has been dismissive of the idea of WETH as collateral, thinking collateral that appreciates in value was far more fun. Nonetheless, we’re happy to see he listened to feedback and pushed a vote.

By the by, for those curious about $crvUSD’s own level of decentralization — every collateral type since the initial test market of $sfrxETH has been subject to DAO approval. Turning over the keys at such an early stage reinforces that Mich is a class act on the subject.

While it still requires some technical sophistication to propose your own new collateral types, the capability to do so is nonetheless fully open to the public. If you have strong interest in adding new markets, you can ask for some tips in the dev channels (or just hold tight for the feature to inevitably hit the UI).

Incidentally, there were some concern trolls inquiring why Curve was supporting WETH and not ETH. It recalls the glorious week from last year when memesters attempted in vain to FUD WETH into depegging from ETH. Needless to say, the immutable WETH contract is used interchangeably with ETH in the Curve backend and UI:

$crvUSD Pools

Outside the world of $crvUSD markets, we also see improvements in the utility for $crvUSD itself.

Thus far, the supermajority of this has been going to Conic Finance, which can throw its weights around the ecosystem through their ominpool concept.

Accordingly, we’ve seen some protocols start to push for their own crvUSD pairings. Keep an eye on these pools, as they may one day ascend to Peg Keeper status.

Frax was the first such pool, and the Conic community is presently pushing the pool and its tempting rewards into its omnipool.

A few new pools are joining the fray. The newest pools to fly the Shrek-themed logo include a couple of stablecoin warhorses.

Stablecoin stalwarts DAI and MIM join the party seeking gauge votes for their pools, presently quite shallow.

The implications for DAI integrations with Curve are substantial. We hope to get time to write a full post on it, but we’ll just tease this for the time being…

Misc

Last notes on $crvUSD is some housekeeping. The fees for $crvUSD have just far just been accumulating, but a burner vote would allow this to start being distributed to veCRV holders. Still nothing substantial, but nice to see.

Secondly, a new controller implementation vote is largely procedural, but we’d recommend it be enacted (not financial advice).

Finally, for anybody who lamented that $sfrxETH was unfairly privileged by being the first collateral, take note that it’s now a liability. There’s some work to be done before its cap can be increased.

For more on $crvUSD, check out this great thread + explainer: