May 11, 2023: Soft Liquidation 🌧️☔

May 11, 2023: Soft Liquidation 🌧️☔

Complete walkthrough of $crvUSD's soft liquidation mechanism, plus $bETH

Set your calendars!

czETH

Don’t let them distract you… there’s a new LSD coming in hot.

Binance’s $bETH is in it to win it. Since launch they’ve accumulated some heavy firepower.

They are also exceedingly eager to birb. According to sauces they will participate in birbing this round.

DefiMoon puts the pieces together with a TL/DR of how it may play out

Soft Liquidation

We agree with Schizoxbt’s take here. We’ve seen a lot of interesting protocols lately using LSDs as collateral — eBTC being one example we highlighted in February.

Unsurprisingly, we’re lately focused on $crvUSD among the cohort of new concepts. Its functionality may be a bit counterintuitive if you rely solely on the white paper or repository, but the past week of “testing in prod” has given us a beautiful real world illustration of how exactly a “soft liquidation” will play out.

Even better, Mich and fam have been all over Curve Telegram groups with useful play-by-play analysis. Sifting out signal from noise in so many Telegram groups can be challenging, so below we organize it all into a convenient narrative.

The short version is that Mich aped into $crvUSD with a million dollar position as close as possible to liquidation price so as to test the performance of his LLAMMA. Fortunately for his experiment, the price of ETH in fact dipped lower during the period. On traditional lending protocols, he would have lost everything if his position sunk underwater.

Instead he describes his experience of being soft liquidated in $crvUSD as feeling “comfy”, experiencing just a 0.5% loss:

Immediately upon depositing, the collateral was spread evenly among several bands. Mich took out the largest possible loan, so these bands were positioned very close to the oracle price, ensuring liquidation would occur upon even a slight price movement.

The actual process of being liquidated is well explained by Fiddy:

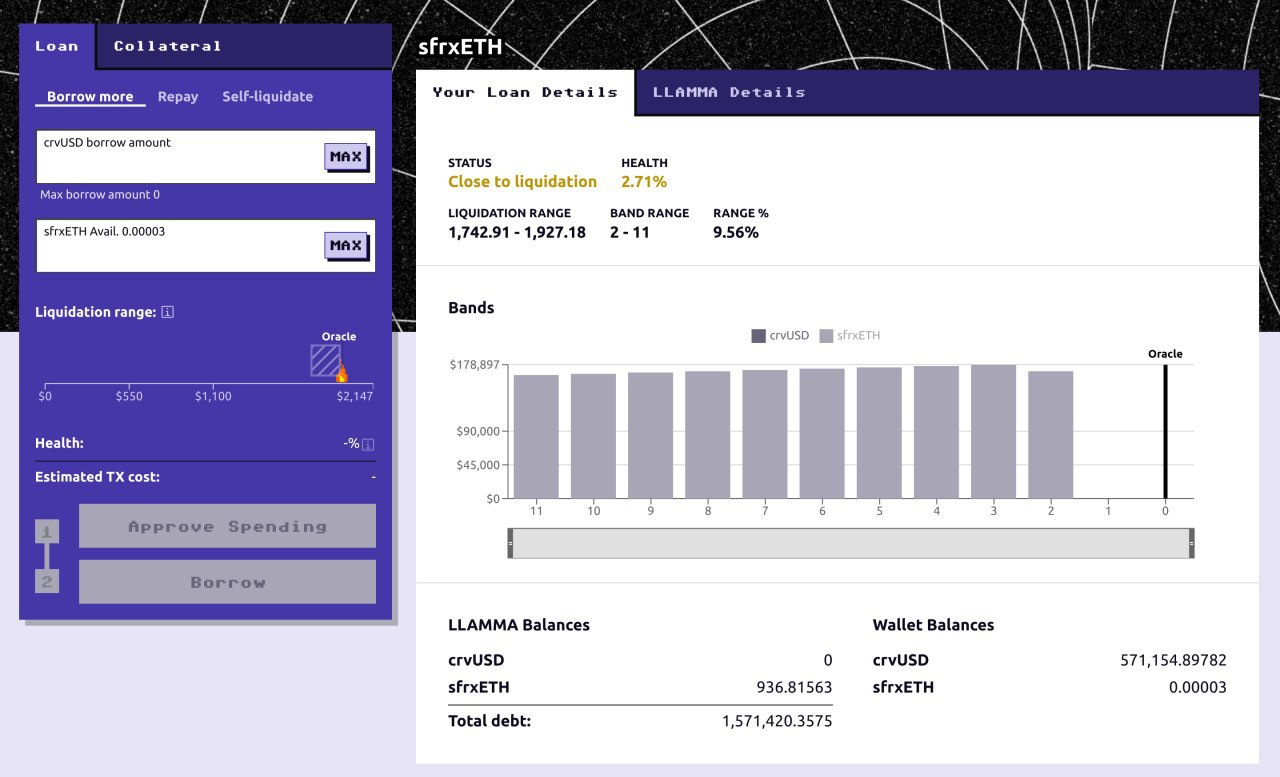

Zooming in on Mich’s screenshot, you can see what his situation would look like in a hypothetical (?) UI. Here is how his position wound up after all is said and done.

In this case the price of ETH already dipped and recovered, so it chewed a bit into the liquidity bands closest to the current price. Band 1 got liquidated. Band 2 shrunk slightly because of the liquidation/deliquidation process.

Another public screenshot captures the effect of soft liquidation in the moment:

Another snapped later shows the collateral within the band almost fully converted to $crvUSD.

The latter two screenshots demonstrate the process of soft liquidation, in which sfrxETH is converted into $crvUSD to protect against liquidation.

In chat, 0xstan creates some helpful visualizations of the process.

If you want to see an example of how liquidation looks on-chain, observe the mental illness of 0xa2ac94f6c483c471cae5a8aecc0a65aa2ca19505b5748320cf435006a5a8ddd9

Of course, the best case scenario is you don’t get liquidated at all. When you play around right at the margin you of course risk getting burnt. We hope degens opt for safer settings where the risk is reduced.

Nonetheless, the actual results here (~0.5% loss, retain long position) are significantly better than you might fare in traditional lending protocols. Usually if you fell asleep and prices dipped down slightly, you get rekt (100% loss, lose position).

Enough about the experience for degens actually using it, how does this money slosh through the rest of the ecosystem? There are a few moving pieces. Most notably, the system relies heavily on arbitrage traders have the ability to make money reinforcing the peg in LLAMMA. They tend to do so when it’s profitable inclusive of gas costs, thus the liquidation/deliquidation of collateral is not necessarily instant.

In slightly more detail:

In this case, since Mich made his deposits, we’ve seen extraordinarily heavy utilization, over 100%.

Eigenphi has put together a great dashboard tracking this activity:

Combining this all into a single pool for liquidations, instead of each individual positions, makes the entire process quite smooth for traders, and creates incentives for users to open larger positions.

Note that for all this arb activity, the benefits accrue to the traders. For veCRV holders, the spice flows not from the arb activity, but from interest rate on borrowing (looks to be near 2%). Our back of the napkin math puts this at a million in annual fees to veCRV stakers for every $50MM TVL that gets added to $crvUSD (we’ll issue a correction if people farther right on the bell curve chastise us).

The Telegram chats are loaded with much more quality Q&A. Recently we caught a good chat about the use of price oracles, toward the end of which Mich describes how $crvUSD was built so it could survive a depeg of one of the aggregated coins used for price.

For more reading on $crvUSD, we recommend starting here and reading for several pages. Most every question gets answered in this span.

If (wen?) the UI goes live you can also get a good understanding of how it works live just by plugging in Mich’s address into “watch-only” mode on your wallet to see how his position shakes out in realtime.

We hope this has been useful. Of course, if $crvUSD does go live remember it remains highly experimental, and playing with lending protocols is dangerous. We always recommend only playing in cryptocurrency with funds you are willing to lose, especially when it comes to new untested protocols.

Even worse, protocols with built-in rug functions!

It is incredible that you put these info into one substack.

tbh, this should be in a paid section 🫡