May 25, 2022: Peggers Can't Be Choosers 🥺📌

Analysis of the Fight to Repeg 3pool, stETH, and cvxCRV

A couple weeks ago the bombshell collapse of Luna made everybody poor and threw markets out of whack. Today we perform a deep dive into the ongoing battle to repeg 3pool, stETH, and cvxCRV.

3pool

In the immediate aftermath of the disaster, the immediate move was a panic flight out of $USDT. This caused what some FUD-sters tried to sell as a depeg, though it looks more to me like an arrhythmia:

As long as Tether processes redemptions normally at 1:1, I have a tough time believing this was a true depegging. I’d call prices that deviated from 1:1 a form of price gouging, but I don’t care to get tied up in a semantic debate.

Whatever you call it, the outflow was real. Tether processed about $10B in withdrawals, dipping its market cap accordingly. Potentially the bleeding is slowing, but the threat of stablecoin regulation is keeping degens wary.

Tether in the meantime released some supplemental materials about its operation to calm nervous investors. The service claims to have over $10B more in reserves than its supply.

Perhaps the most bearish indicator for Tether is that USDC Bull has apparently lost allegiance to the other half of 2pool. The top trader of 2022 has seemingly dropped the Tether “green bull” cartoon from its memes, last appearing on May 9.

As for Curve’s flagship 3pool, the pool’s outflow has reversed and seen some liquidity trickling back in. The pool is gradually edging upwards in volume following the plummet. This is manifesting in the form of a slight drift back towards peg.

Curve’s pool currently has a very high A value, meaning even at this level of imbalance, the peg is relatively tight. At the moment, 100 bucks worth of $USDT will buy you 99.87 in $USDC, less than a typical ATM fee.

Some users inquired what level of activity it would take to imbalance the pool from here. In order to depeg the pool, it will require billions of dollars worth of activity. The following chart shows the effect on the peg as users make a large deposit of Tether into the pool (which would have the effect of imbalancing it).

The x-axis is in units of 10 ** 10 (aka $10,000,000,000, or ten billion dollars). A deposit of $10B Tether, about 14% of the entire $USDT supply, will be enough to knock the pool about 20% off-peg. Unlikely, but stranger things have happened.

You can download the Brownie script to generate this if you’d like to play around with the numbers yourself.

We discussed at the time how whales could use Tether’s 1:1 redemption to arb this pool back towards balance. In practice there’s some TradFi friction that renders this a bit slower. Hence, Curve has submitted a gauge vote to reduce the A parameter to promote this arb and push for a repegging.

The governance vote has passed, but it will take a few days for the ramp to complete. We’re likely to see the pool remain near this current level of balance in the interim.

stETH

The stETH pool, now Curve’s largest by TVL, also took some action to reinforce its peg. In this case, they created the “Concentrated stETH” pool to offer bonus rewards to the excess stETH floating around.

In terms of attracting attention, the concentrated stETH pool was a big success. Within four days the pool jutted up against the $600MM TVL mark, fairly fixed at the desired 13:1 ratio.

However this has apparently failed to have much impact. The stETH pool is presently at about a 30-70 imbalance, meaning 1.00 $stETH buys you 0.98 $ETH.

This carries a bit of a lesson for pool creators: adjustments to the A parameter can only go so far in shoring up tokenomics.

It’s an open question whether or not $stETH should actually trade so close to $ETH with the merge on the horizon. In the merge, the use case of the two tokens will diverge.

Lido has a rather full plate at the moment. In addition to any moves they’ll be making to shore up their core Ethereum pool, they also have been dealing with the fallout from half its business disappearing in the Terra collapse.

For those curious, their community recently opted not to support the reboot.

This all comes as RocketETH has been scrapping to gain market share in the ETH staking wars.

The trendline has been ever so marginally upwards for Rocket Pool over the past week, though not at pace to make a significant dent in Lido’s multibillion dollar lead before the merge.

$stETH cap flat

$rETH cap inching upwards

For more info on the differences between $stETH and $rETH, check this thread on the differences:

cvxCRV

The $cvxCRV token dropped a bit last week, amidst an interesting time in the Wrapped Curve Dustup. As of publication this has drifted back, and 1 $cvxCRV will buy you 0.973 $CRV.

As you can see, the pool suffered a bit in the collapse, but staying within bounds at the more extreme end of its typical trading range.

The consequences of a complete depeg between $CRV and $cvxCRV was outlined in a recent Convex FUD thread.

For our sake, while we always like to consider the case against our priors, we remain relatively unworried. Convex earmarks a steady portion of its fees to incentivizing this cvxCRV pool. When markets turn particularly bearish and yield sources elsewhere dry up, this can have the effect of boosting yields in the pool, thus attracting liquidity from speculators.

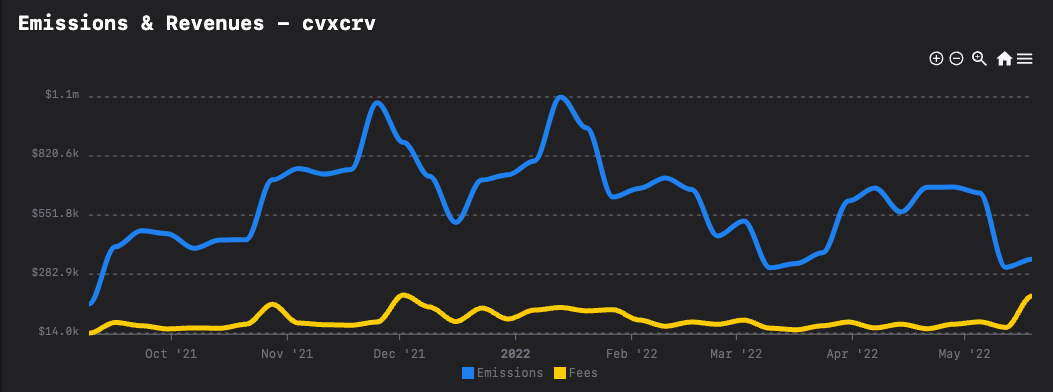

The fees (yellow line) have been quite juicy lately for people willing to sit in the pool and wait out the storm.

The above chart’s blue line might appear bearish, but is a bit misleading in that it’s dollar denominated. All DeFi prices took a dump lately, as did the pool’s TVL. When the denominator dips and the numerator ticks up, it’s boolish for farmers.

In percentage terms, the 35% boosted rewards is on the higher side of rewards for the pool lately, and we might see liquidity flow to the pool to take advantage of these yields. 35% on Curve means some of the other services can autocompound even higher gains. For reference, Llama Airforce clocks in at 53%.

Of course, my flywheel bullishness may properly read more as textbook mental dysfunction, and certainly not financial advice. If you dumped your net worth into $CRV at its speculative peak you’ve lost about 85% of your life savings. Always, always, consider the bear case.

Bonus Data

If you made it this far, we assume you like charts and number. Here’s some interesting data floating around, some of which may make its way into future articles:

Finally, for degens who prefer JPEGs to Curve pegs, keep your eye on the JPEG’d auctions of several punks that got liquidated in the madness. We expect a flurry of activity at closing time, given the ~50 ETH floor price for the iconic collection.

Disclaimers! In addition to flywheel maximalism ($cvxCRV, $3CRV), author has exposure to assets referenced in the article including $stETH, $LDO, $DPX and $JPEG.

Stellar analysis. Thank you.