May the 4th, 2022: We Like The Free Pool 3️⃣➡️🆓

May the 4th, 2022: We Like The Free Pool 3️⃣➡️🆓

@nagaking Study Recommends Slashing 3pool Fees

Somewhere between the 4pool and the 2pool, sits the classic 3pool.

One of Curve’s best innovations as it has grown has been morphing 3pool from a driver of early trading volume into a critical building block in DeFi infrastructure. The 3CRV LP Token today serves as the base layer of dozens of other Curve pools, providing unmatched liquidity and flexibility for any DeFi stablecoin native.

The future may well see 3pool dominance eroded by 2pool, 4pool, or other based pools. Rather than simply becoming obsolete, 3pool and its $3 billion in raw liquidity is evolving to serve the current state of DeFi.

The latest developments are spurred by a shock study from the fabled @nagaking. His modeling shows that slashing 3pool fees would actually boost overall returns.

Not having seen the raw research, we’re at the mercy of the topline summary. The results appear to support the argument that 3pool is more valuable as a base layer than a trading pair.

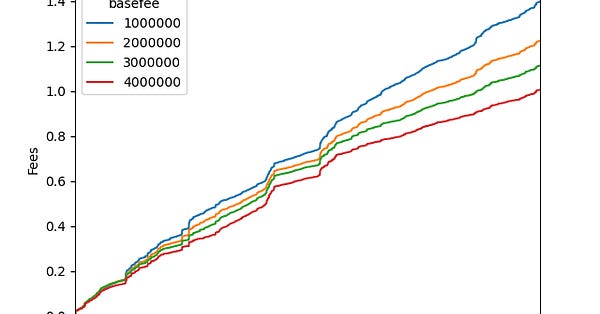

This chart demonstrates the effect of dropping the 3pool fee leftwise along the x-axis. The base fees in green, already quite inconsequential, tick down slightly. However the theoretical volume generated by other fees more than offsets the decrease.

The taste of the study we’ve seen raises further questions. For one, we’d be interested to review prior results of cutting from 4bps to 3bps.

It’s of course tough to parse this data cleanly, but one might look for discontinuities in whale behavior relative to shrimp, whales being more sensitive to trading fees than gas costs. Another private tweet in the thread by a famed DeFi founder also inquires about the effect of gas costs. Anecdotally, it looks to be around $1MM sized trades where the fee starts to exceed gas price, so any transactions under such a threshold may show less sensitivity.

At any rate, the decision has already been sent to governance to decide, where the debate is coalescing into two schools of thought.

The first school of thought is to ratchet down slowly — try 2 bps and confirm the effect, then drop further as needed.

Another way to articulate this argument: a competitor calling themselves “Uniswap” tried and failed to kill Curve by undercutting 3pool with a 1bps fee. Since Curve has successfully protected its higher margin product, why not hold onto this advantage?

The other school of thought is to cut deeper — drop below 1 bps and even scrape 0.

There’s also a sinister brilliance in cutting to 0 bps. Should Curve decide to engage in a race to the bottom, it’s notable that Curve would theoretically increase profits on the way down. Uniswap’s gambit appears to be more of a loss leader. Uniswap pushing to 0 bps would cost them money. Why not lean into Curve’s unusual moat here?

Then again, Uniswap has nearly bottomless access to VC money, and VCs have shown no hesitation about lighting money on fire in their increasingly quixotic attempts to erode Curve dominance.

Curve OGs may recall as far back as last year, when Uniswap was allegedly planning to eat Curve by ::checks notes:: undercutting 3pool. Seriously, VCs may be the next job displaced by technology whenever somebody gets around to building an AI bot that generates bad takes.

Naturally, the legacy press had a field day, generating endless thinkpieces and kaffeeklatsches prematurely crowing about the premature death of Curve. Curve for its part laughed this off and focused instead on growing out its v2 pools, which already constitute nearly half of volume and growing.

The 3pool, by contrast, is under 10% of volume and unlikely to become a serious contributor. Trading between USDC and USDT will never be a big money-maker in and of itself.

This post hints at the value prop — when I get 3pool tokens from various activity around the flywheel, it provides great optionality. It feels safer than any constituent coin, because there’s theoretically less depeg risk. I can unwrap easily to any token if I need. Until then, if I accumulate enough of a stash, it has a ton of capability to restake in other Curve pools for higher yield. Never once have I considered staking into the 3CRV Gauge.

Of course, the clear downside to cutting fees is that holding 3CRV in and of itself becomes closer to holding a dollar. Fewer fees means less implied interest.

Then again, if you’d held 3CRV since inception, you’ve only earned ~2% in fees according to the virtual price. While this beats the boomer basis points you can get in a bank account, either way you’re rekt by inflation.

I’d assume nobody is holding 3CRV as an inflation hedge. So why not shake things up? Seems like a good chance that CRV stakers would get more 3CRV earning slightly lower fees, overall it feels like a win.

Whatever the results, it’s wonderful to see 3CRV adapt to changing market conditions. 3pool looks like it will continue to play, even as we see increasing adoption of other base pools.

The author therefore endorses progressively slashing 3pool, to 1 BPS and eventually approaching 0. Mostly because the author is a mentally unstable stablecoin enthusiast who enjoys aggressive action.

Fortunately for jurisprudence, the author has little voting power, and you can easily counteract his influence if you disagree. Do your patriotic duty and VOTE!

Disclaimers! Author is a mentally unstable stablecoin enthusiast with 3CRV LP Tokens.