Octover 3, 2023: Through the Looking Glass 🐇🍄

Alice's Adventures in Optimizing the wstETH-rETH-sfrxETH TryLSD [sic] pool

An excerpt from Lewis Carroll:

In the digital wonderland of Curve, where numbers frolic and parameters gambol, a peculiar pool named TryLSD caught Alice's eye. It was a garden of Liquid Staking Derivatives (LSDs), each a colorful petal in the blockchain bouquet. The Cheshire Cat, with a grin, presented a governance proposal, a scroll of change to beckon more volume and Total Value Locked (TVL) into the enchanted pool.

Alice peered into the reflection of the pool, where old parameters morphed into new. The Queen of Hearts, with a flourish of her scepter, heralded the new parameters, each tweak a step into a realm of reduced slippage, a dance of liquidity with lesser fee. Amidst the whispers of governance, the numerical characters frolicked, revealing a tale of enhanced liquidity and competitive fees, a narrative spun by the wizards of the community.

As Alice delved deeper into the TryLSD narrative, amidst a cascade of numbers and letters, the garden of Curve bloomed with promise. Each new parameter was a note in a whimsical symphony, orchestrating a melody of enhanced liquidity and lower fees. The Mad Hatter, with a tip of his hat, invited all to partake in the governance fest, a celebration of communal concoction to shape the essence of the TryLSD pool.

The tale of TryLSD was a lyrical lore in the grand narrative of Curve's governance, a stanza in the endless poem of DeFi's evolution. And as Alice wandered through the numeric foliage, the essence of community governance rang through the wonderland, a melody of collective endeavor in the whimsical world of blockchain.

Get ready for some trippy, far-out colors as we triple our dose of LSDs… (liquid staking derivatives, of course)!

This past week, Nagaking and ON-DeFi teamed up to run some optimizations on the parameters of the TryLSD [sic] pool.

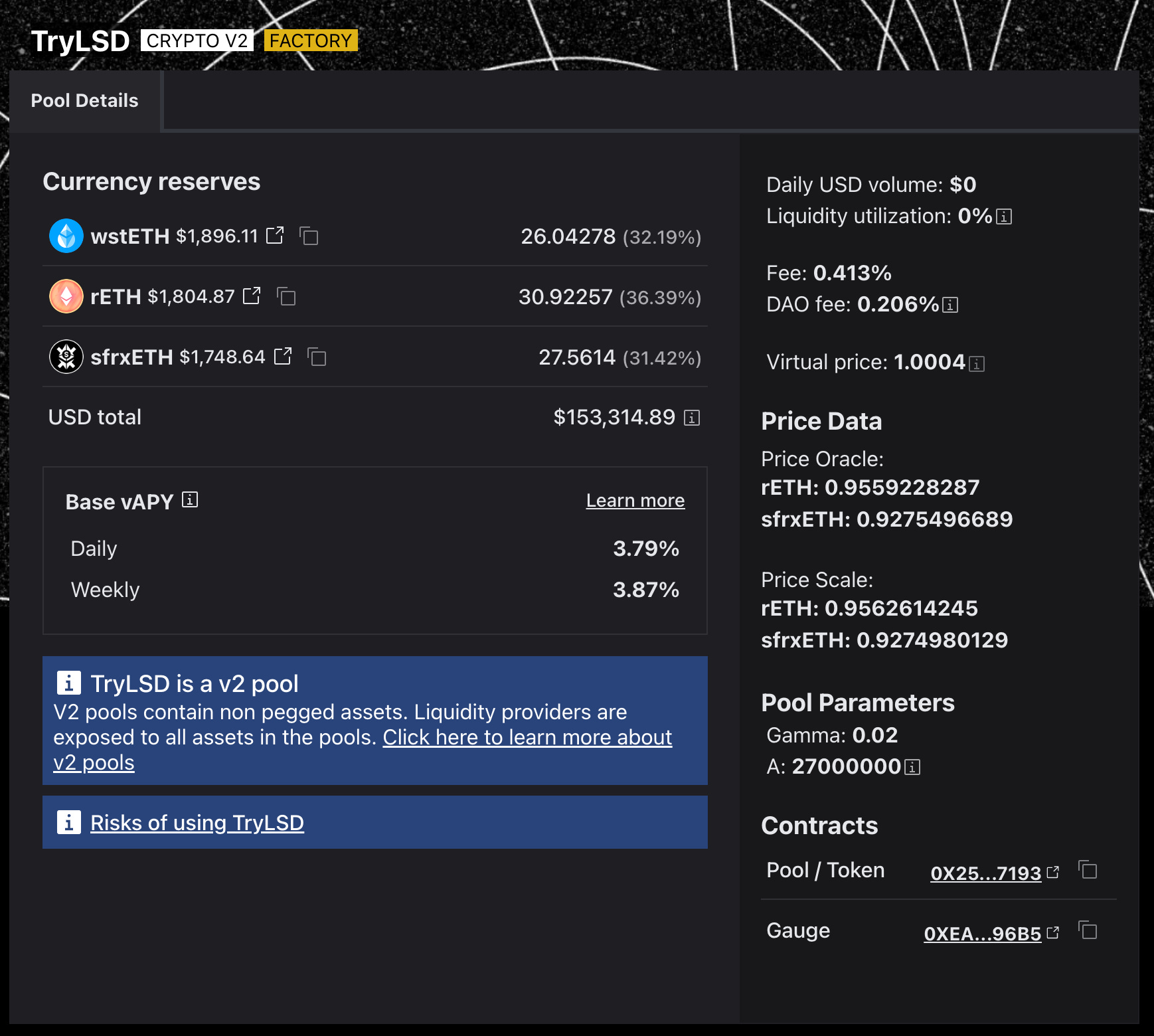

The TryLSD pool is intended to facilitate transactions among three major Liquid Staking Derivatives: $wstETH, $rETH, and $sfrxETH. LSD-Fi has been one of the few major narratives to emerge over the past year, so the pool could become quite a major trading hub for Curve if it gets off the ground.

There’s good precedent for such a pool as well. Balancer has a similar pool that does fairly well, with a 4 bps fee. No reason why Curve’s pool can’t be similarly successful.

The TryLSD pool is a Curve v2 pool, which contains two different types of fees… a mid fee when the pool is balanced and an out fee when the pool is imbalanced. It therefore won’t necessarily be competing directly on fees, as it may be looking at ranges between 1-5 bps.

The Curve pool happens to be floating near a 4 bps fee, but liquidity is extremely shallow at the moment — just $153K in liquidity.

Naturally, the proposal includes a gauge vote, which would help incentivize this pool to achieve deeper liquidity. Without deep liquidity, impossible to make trades without massive imbalances. Yet tough to attract liquidity for each of these assets, as they have a lot of potential destinations. For instance, LP-ing $sfrxETH into this pool means not lending it for $crvUSD with its good returns.

The real interesting part is not so much the gauge vote, but the parameter exploration.

The first step in the analysis was to vary over the pool’s parameters. The overall space in these graphs shows gamma on the x-axis, which represents the overall breadth of the bonding curve (which affects the curve at more extreme values), and fee_gamma on the y-axis, which controls how quickly fees change.

Here the intent is to vary over this parameter space and look at what the most effective range of fees happens to be for those parameters. The target, per above, was about a 5% fee to compete with the open market rate, which is signified by the yellow diagonals.

From here, they iterated over this same space to check the effect on other key metrics. Shown in order in the next four graphs: annualized returns, liquidity density, trading volume, and pool balance.

Some optima here were discarded due to the poor user experience. For example, in the first chart in the top row showing annual returns, it shows up brightest in the chart’s upper right hand corner. However, if you look at the third chart (first in the second row) of pool volume, the actual trading volume in this area is quite poor.

For these parameters, the higher liquidity density was driven by prohibitively high fees for off-balance trades, preventing traders from imbalancing the pool. Thus, the high liquidity density came at the expense of limited trading volume

The overall winner was chosen as the bottom right corners of each chart, ie the bright yellow part of the third graph (volume). In this region you could hit a comfortable max for most of these metrics:

returns: ~15% annualized

liquidity density: ~28

volume: ~11K ETH

pool balance: ~7% from balanced

The average fee was 4.6 bps, a bit above the competition, but it only hit the higher values on a few major outliers. Most of the time the pool proved to be quite balanced and fees would be low under ordinary circumstances.

Finally, they took a look at changing the pool’s half life. Noting that most of the time LSDs prices hold fairly steady, punctuated by only occasional shocks. Increasing the half life here would have the effect of smoothing out these price shocks. At present it was set at the default of 600 (10 minutes).

These charts show four key metrics and the effect of increasing the half life from 10 minutes to over an hour.

All of these show improvements at the higher half life. Plotting this over real historical prices, you can see the effect is pronounced.

The major dips in the last two charts occur on the purple line (with the currently shorter half life of 600) caused by sudden volatility that tends to get erased in a longer half life.