Apr. 7, 2022: Proudly Built on Curve 👷🏗️

Apr. 7, 2022: Proudly Built on Curve 👷🏗️

Latest from Concentrator, LendFlare, Paladin, Conic, cCRV, Curvance

Back in the Web2 days, projects would affix a label to the bottom of their site: “Proudly Built in <city>.” With Web3 making location all but irrelevant, perhaps soon they’ll read “Proudly Built on Curve.”

So many protocols are using Curve as the base layer these days, it’s been difficult to keep them all straight.

We’ve already profiled some of these in great depth, some just a cursory overview.

Herein we’ll provide a quick update on their current progress. We’ll use araphel.eth’s list as a guide. We’re only considering projects that are early launched or pre-launched, so we don’t consider more established projects like Votium, Redacted Cartel, or the Union. @araphel also cites Concave, but we see this as more as the Convex of OHM than a piece of the flywheel, so we’ll also omit this (unless readers request otherwise). A hearty thanks also to the more comprehensive background on this by TokenBrice.

We present projects in descending order of the project’s current status (launched to idea). The author has not yet used any of these projects, and none of this is a formal endorsement. Never financial advice and always do your own research, especially with newer protocols!

Concentrator

At the top of the pack in terms of TVL is Aladdin DAO’s Concentrator, which has claimed $63MM TVL already since its launch.

The team’s autocompounder has found a clear niche — everybody likes Convex, why not Convex on steroids? The concept of automatically harvesting and restaking your $CRV rewards for $cvxCRV rewards is easy enough to understand and represents free money for yield farmers. Would you rather have juicy rewards, or the same juicy rewards plus ~50%?

Many new users take a wait and-see approach to new smart contracts since it’s difficult for even experienced coders to identify bugs. The team is smoothing over this process with two audits.

The minor issues turned up by the two audits include the potential for an MEV attack on rewards and the rug risk of a 6/9 multisig, which have been discussed with the team.

The team is not planning to stop at the Concentrator. They’ve long hinted that “more is coming” and have already teased they are pushing to several chains.

At the moment their wrapped Aladdin cvxCRV ($aCRV) token looks like it’s primarily used for accounting as its withdrawn to other tokens before withdrawal, similar to Union CRV. If $aCRV eventually finds its way into more interesting tokenomics, it would seem to be a good fit for a future v1 or v2 Curve pool.

LendFlare

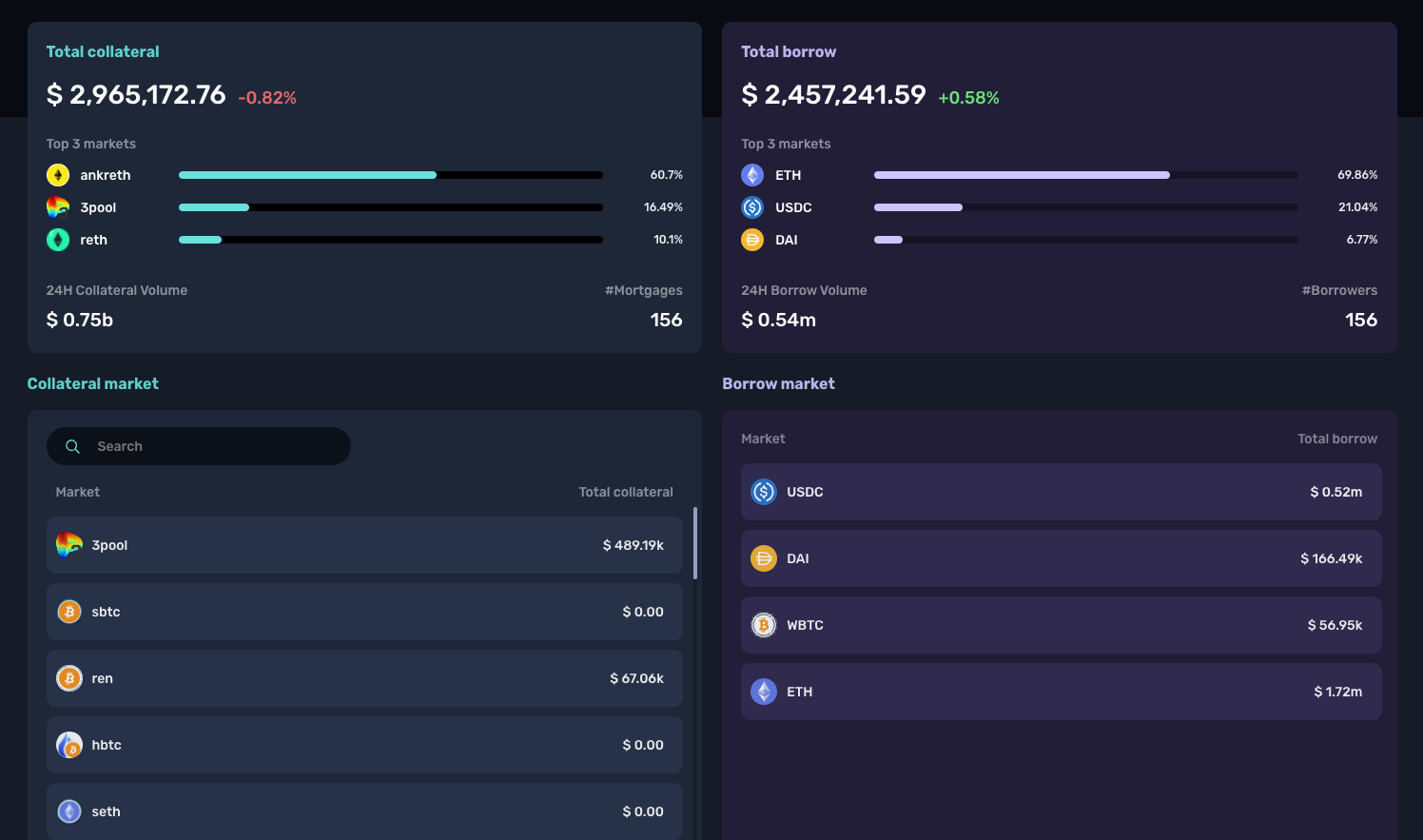

LendFlare may be the most underestimated of the new platforms. They popped onto our radar in December, and already built and launched an elaborate and functional collateralization/lending platform, similar to Aave, for Curve LP tokens.

They take second spot on this list with a total $37MM locked, including $3MM collateral, $2.5MM borrowed across 156 mortgages. They quote $0.75b 24-hour collateral volume, (which we assume is millions, not billions.)

LendFlare is notably friendly to users who choose to collateralize their assets. Users who collateralize continue to earn Convex rewards. This is clearly useful for users who want to both stake and use ETH, and unsurprisingly we see ankrETH and rETH are the most collateralized coins already. Here LendFlare has a good opportunity to integrate Concentrator (or build a competing service) to boost these yields further.

To protect against liquidations, users can only borrow like-kind assets (ie ankrETH → ETH) and have to pay a 0.1 ETH deposit, with the borrowing rate described in their docs. Loans have repayment windows, and trigger liquidations if they are not repaid.

They also completed their $LFT token IDO. The $LFT token is designed very similar to $CRV, with 3.03 billion total supply and staked veLFT earning 50% of interest fees.

The token was initially trading under $0.01 but since ticked up to $0.04. Their recent airdrop is released slowly over the course of 4 years, so the token may be somewhat more resilient to the farm-and-dump pressure that follows so many new IDOs.

A fantastic thread by @kamikaz_ETH covers the bull case for the $LFT token, vis-a-vis Curvance and other trends.

Another utility of the $LFT token inspired by Curve is the capability of boosting $LFT rewards on supplied assets. At the moment these rewards are quite substantial. However, with very low TVL so far, we are sure they’ll fall to earth as more users find their way to the platform.

One red flag is that the main source of their token’s liquidity is a Uniswap pool. The $LFT token would be a perfect fit for Curve v2. Somebody has taken the trouble launch an unfunded LFT/ETH Curve v2 pool though, so perhaps the team has plans afoot.

Paladin

In the early shipping stages is Paladin. Paladin is providing value to governance tokens with a variety of functionality. Given the broken state of governance in so many DeFi protocols, this is badly needed. In particular, their Warden product may be of interest to veCRV stakers with its capability of buying/selling veBoost.

The team launched their $PAL token late in March, and they already have a viable Curve v2 pool with $2MM in liquidity.

The team is hard at work with establishing their early tokenomics and pushing decentralization as their token starts to hit markets.

April could be a big month for Paladin.

The Paladin team is demonstrating outstanding execution and solving a big problem that runs directly through the Curve Wars and has the potential to bring more decentralization to all of DeFi. Definitely worth keeping on your radar!

More details via this recent podcast, which is summarized in thread form here:

Conic Finance

Conic Finance is pre-launch but at the public distribution stage. We covered the mechanics last Friday so we won’t review them heavily here.

We have to note some recent controversy around Conic. Yesterday giga-whale @Tetranode sounded a note of caution.

The team’s response raised further questions

We have no particular insight into this project, so we won’t speculate whether it’s pump-and-dump, rug pull, or merely sloppy execution. Going forward, our comments about the project will assume it turns out to be benevolent. If it’s malevolent, then it’s of course moot.

Should the project fulfill its promise, it would indeed be a useful and unique lego within the flywheel ecosystem. The capability of staking a single asset to generate the best yield would be popular if executed correctly. Their Github remains sparse so it’s too soon to see how they would address some of the complexities in architecting such a solution.

The community raise was announced on its Medium, and the team has since announced at least 60 ETH was raised. As of publication their token reports 4.1MM current supply on 10MM total supply.

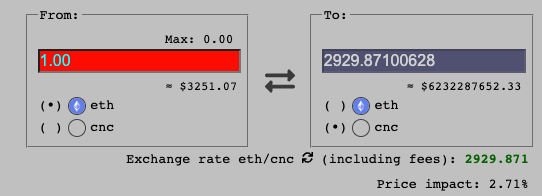

Notably they have both a small CRV v2 pool and a Uniswap pool so early traders can play arb games. On both sites 1 ETH will get you about 3000 $CNC.

In contrast, on their fun airdrop page, 1 ETH will only get you 654 $CNC.

The project has tremendous potential, so we hope they push through the early growing pains and make good on their lofty ambitions.

cCRV Finance

Another new Curve hopeful is cCRV Finance, which describes itself as an L2 for Curve. Built with partnership from Congruent DAO, a successful launch of cCRV Finance would create a 3CRV pool (CRV, cvxCRV, cCRV) that would further help to reinforce the cvxCRV-CRV peg. For more details, refer to the initial @tokenbrice article or this opus by 0xOuija.

cCRV is at the stage of trying to work its way through Curve's governance. Curve governance puts a lot of scrutiny on projects.

With so many open questions about the first proposal, the cCRV team is redrafting and we look forward to seeing their second draft.

Curvance

Of the projects detailed in this article, Curvance was among the earliest when they popped up last December. They boast a high caliber team, however they’ve bene mostly quiet and building behind the scenes so there’s not been major updates in the intervening months.

Curvance is a bit of a competitor to LendFlare, though they focus more on wrapped assets (ie cvxCRV, bveCVX) than LendFlare’s focus on LP tokens. We have to imagine the launch of LendFlare has lit a bit of a fire under the team, and we’ll keep you updated if any new announcements emerge.

That’s that! We didn’t have time to cover some of the protocols cited in the comments to @araphel’s thread, but curious users may further want to check out BENT Finance and XBE Finance. We look forward to seeing this universe expand further, as well as your comments if you’ve tried any of these protocols, and especially correcting any mistakes we made here!

Disclaimers! Author is eligible for the LendFlare airdrop.