February 12, 2024: TryLSD 🐇💊

You Might Like It

The immutable name of the TryLSD [sic] pool may be an unfortunate hit for those of us who advise temperance, but we can still appreciate the unique chemistry of this pool.

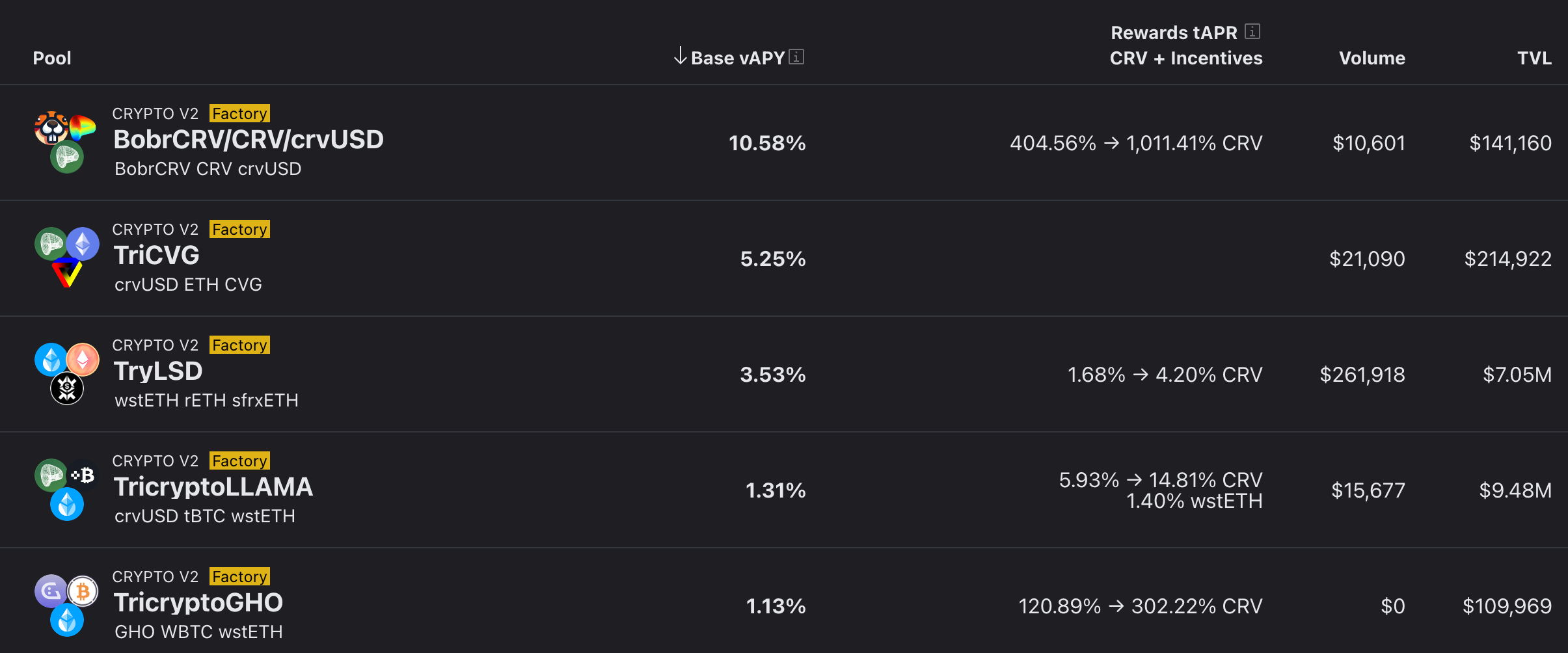

We happened to catch a snapshot of this pool flexing the other day.

Degens may not often consider the Base vAPY on Curve, given that returns are often dwarfed by tAPR incentives. But TryLSD is consistently returning very good base fees.

Reverse sorting all Curve pools by the daily base vAPY shows two lower liquidity pools, where hefty vAPY can come just from an influx of volume, followed by the TryLSD earning 3% (despite higher TVL.)

Break this down and you can see two effects here. For starters, a portion of this is because all three tokens natively earn the benefits of rebasing. The three tokens in the pool all earn native, so the pool vAPY will be healthy.

Aside from the native yields, it also just happens that the pool gets good trading volumes.

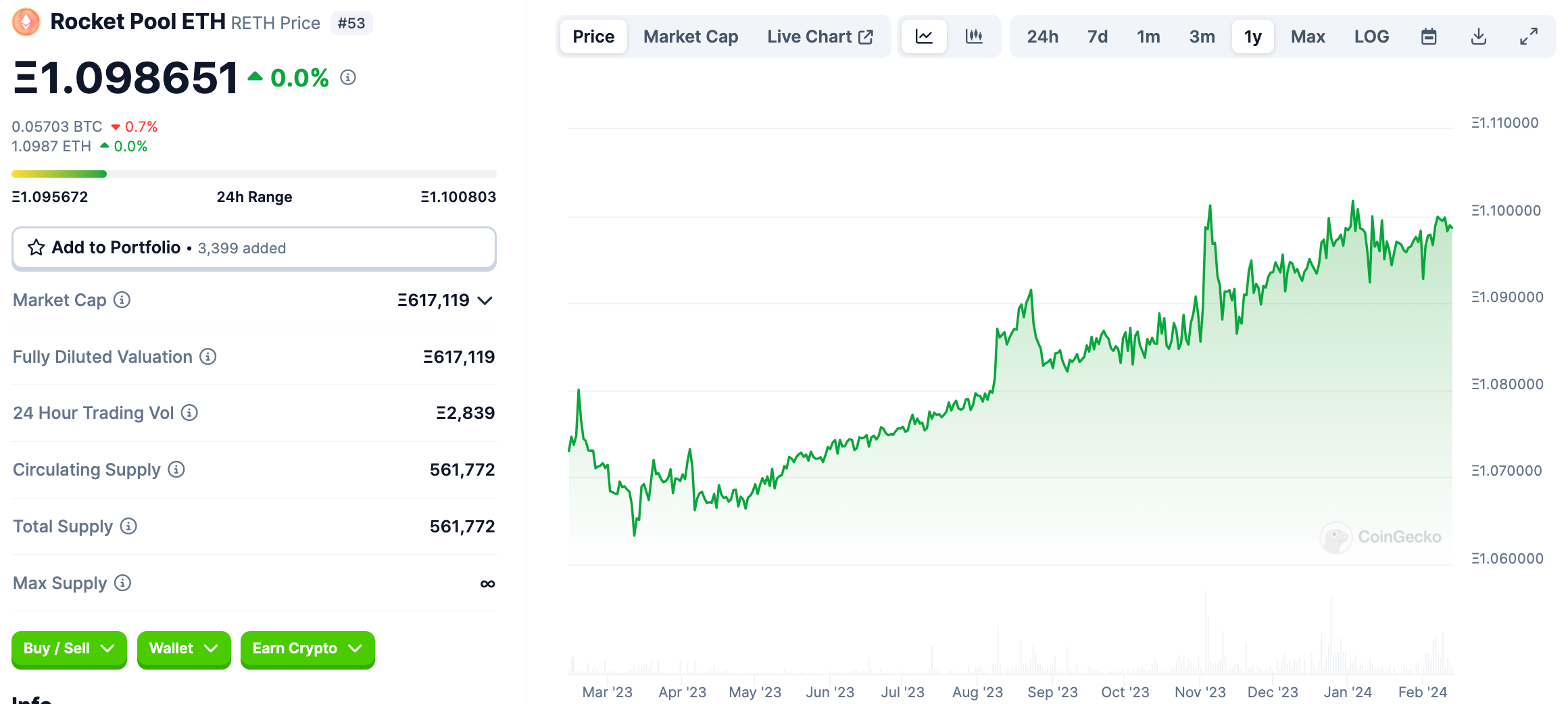

Although the three tokens in the pool are all Ethereum at their core, it’s not *quite* sufficient to treat this as a pool containing three assets with stable prices against each other. The past year of trading shows what a long strange trip it’s been.

The trendline for the three assets are of course similar, but the individual journey is quite different. The variability in spot pricing will always create fodder for arb traders.

One might be able to simply dump a pile of money onchain into the dumbest of smart contracts, and arb traders would have incentive to trade the pool back to peg if the price is wrong. If such a contract is sufficiently dumb, though, then the pool has not optimized liquidity well enough to keep up with price fluctuations. The result would be a pool that works, but isn’t quite so efficient as LPs or stakeholder may hope.

Curve v2 pools automagically deduce the spot price of their internal assets and reconcentrate pool liquidity around these prices. This has some nice effects that work to the benefit of users trading the pool. Traders can make relatively larger trades when the pool is balanced, without so much slippage as a naive pool.

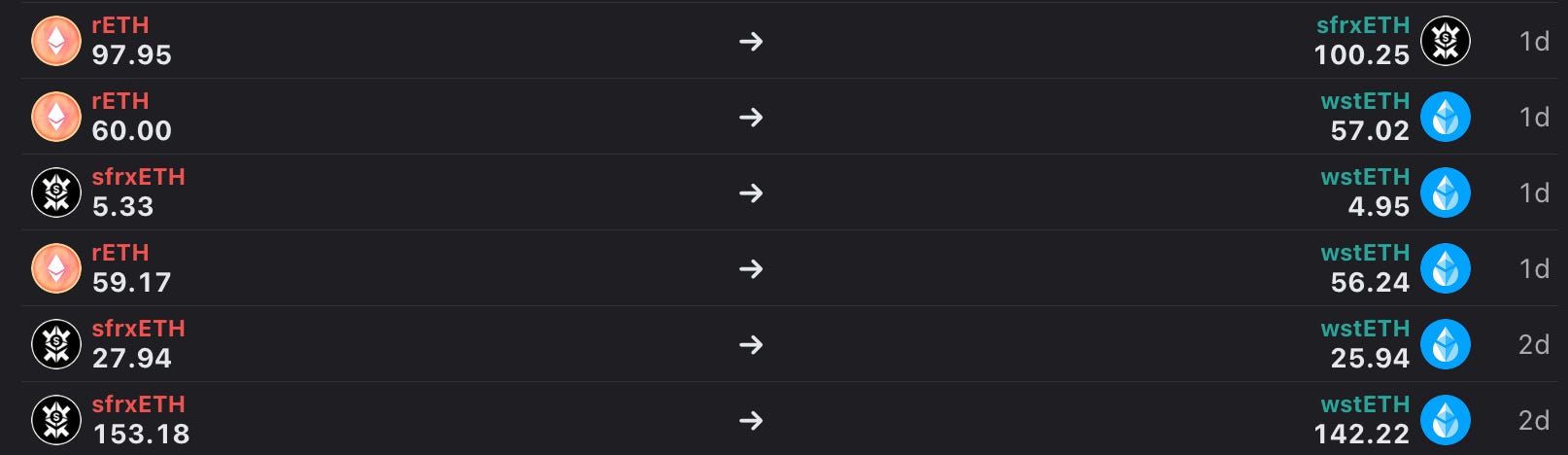

We therefore observe TryLSD is often the beneficiary of large-ish trades getting routed through the pool.

Being capable of handling large trades by efficiently concentrating liquidity leads to efficient utilization. The initial screenshot in this article captured 13% utilization, but in recent weeks the pool’s been spotted with utilization as high as 60% and we suspect even higher.

For comparison, a rival AMM has a similar pool containing three LSDs has about twice the TVL of the Curve TryLSD pool.

You can note a few interesting comparisons. The Total APR of 2.7%-3.8% in this pool accounts for the aggregate of all yield. It breaks down into 0.7% → 1.8% from incentives, 1.87% from rebasing yields, and a mere 0.12% from trading fees.

Curve pool breaks this out as vAPY (which includes trading fees + rebasing yield, currently 3.5%) and tAPR (incentives 1.7% → 4.2% boosted). In total, it would be an effective 7.7% maxed out.

If we were an LP, we’d TryLSD, but this is of course not financial advice. We’ll ignore the superior rewards tAPRs, since it’s paid in $CRV which trolls warn us will death spiral to $0. We’re alone keenly interested in the raw trading fees for the TryLSD pool that are also consistently outperforming, thanks to concentrated liquidity and the variable fee.

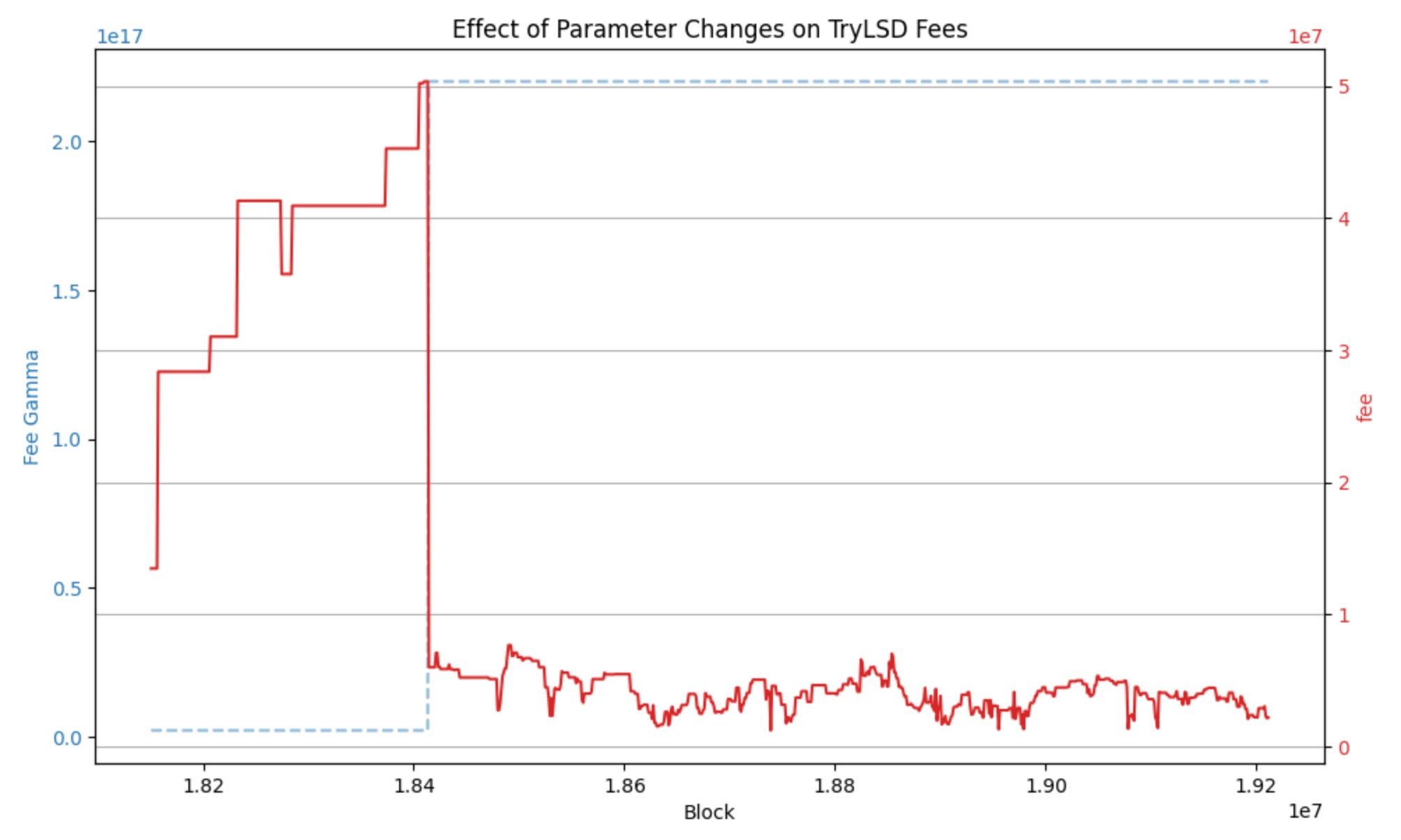

The variable fee in Curve v2 pools adjusts depending on whether or not the pool is balanced. When imbalanced it charges a higher fee, as a way of effectively taxing arbitrageur profits and redistributing some to LPs. When the pool is balanced, it lowers fees so that generic trading fees are competitive.

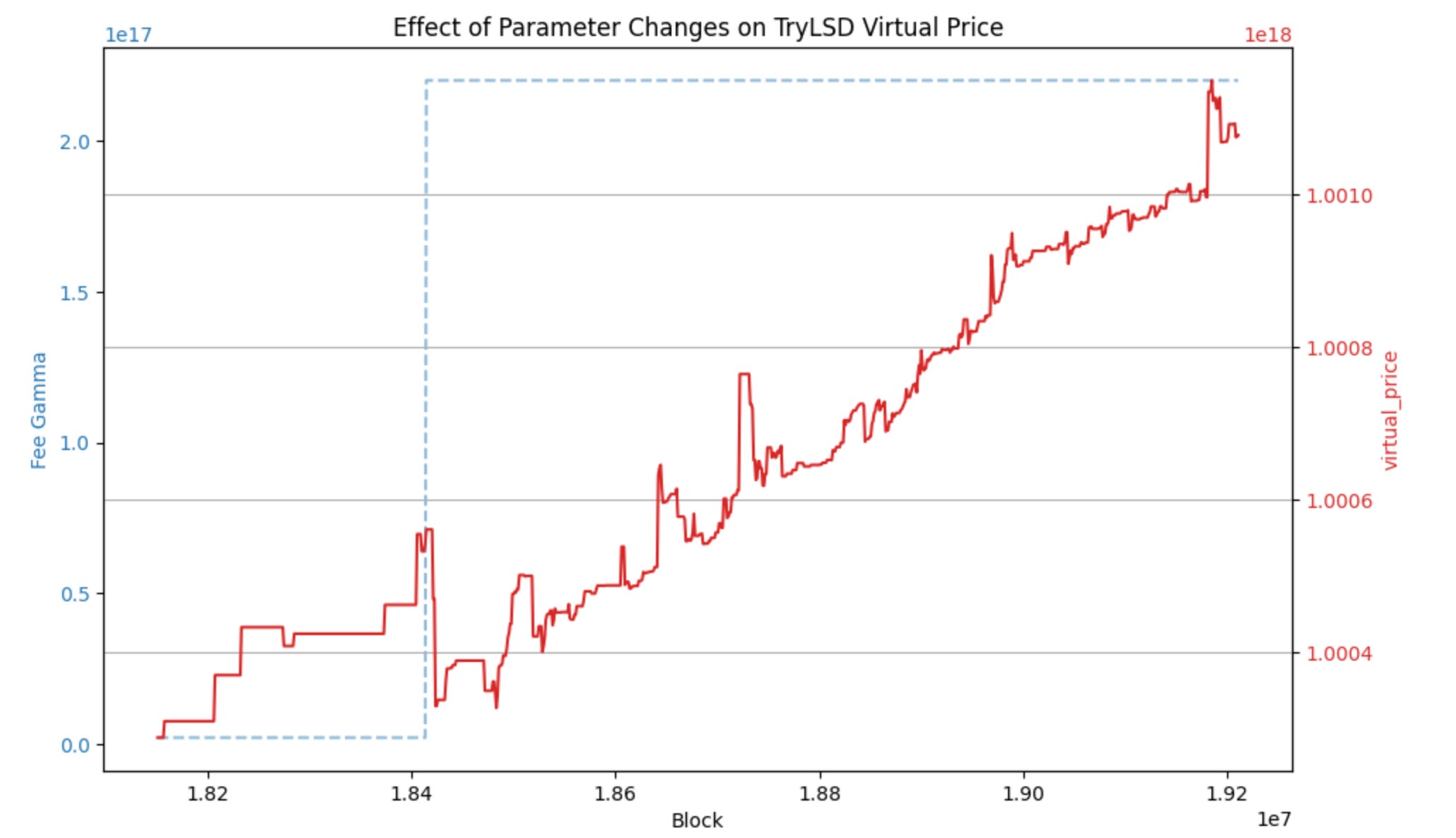

These fees were the subject of significant tweaks several months back around the creation of the pool. An advantage of the v2 pools is that they have so many relevant parameters that can be adjusted to optimize performance.

Octover 3, 2023: Through the Looking Glass 🐇🍄

An excerpt from Lewis Carroll: In the digital wonderland of Curve, where numbers frolic and parameters gambol, a peculiar pool named TryLSD caught Alice's eye. It was a garden of Liquid Staking Derivatives (LSDs), each a colorful petal in the blockchain bouquet. The Cheshire Cat, with a grin, presented a governance proposal, a scroll of change to beckon more volume and Total Value Locked (TVL) into the enchanted pool.

After adjusting the pool parameters, the typical fee on the pool dropped quite significantly, at present generally between 2 to 3 basis points.

The resulting effect on the pool’s virtual price has been quite apparent.

Although the pool is healthy and performant, we may be a ways away from TryLSD cracking the top 10 in terms of revenue.

These pools are mostly dominated by pools with far more liquidity (typically over $20MM). With TryLSD at $7MM, the only other pools of comparable volume in the top ten are CVX / ETH ($11MM) and Prisma / ETH ($4.7MM). For both of these pools, the token pairings are relatively volatile, and they serve as major sources of onchain liquidity, so we’d expect more trades.

Trading between LSDs is also a bit less popular than trading between LSD and raw ether. All the same, a TryLSD pool might be a comfy spot for LPs, which earns yield on all three native assets. It may even grow in size if the pool gets integrated across future Curve products (LlamaLend anyone?)

Overall, the effectiveness of Curve v2 pool performance might be worth keeping an eye on as we observe the emergence of Restaking as a narrative…

Disclaimers! Author has never done LSD and neither should you, kids, but author does partake in TryLSD LP-ing.