January 4, 2024: Four Score 4️⃣🎂

January 4, 2024: Four Score 4️⃣🎂

How Curve stacks up on its fourth anniversary...

Happy anniversary… and what a phenomenal four years it’s been!

Curve is undoubtedly a best in class cryptocurrency protocol in terms of innovation, activity, and all the metrics by which one might rationally hope to judge a token.

…except that the market has a fetish for memecoins with no viable business model… 🤦

The above post attracted a response

At risk of feeding the trolls, let’s break this down point by point…

What are it’s [sic] assets:

Curve has amassed on an enviable multimillion dollar war chest.

Recently, when unable to recover hacked funds, Curve was able to repay victims of the Vyper exploit entirely out of pocket.

Does it have any protectable ip?

Swiss Stake owns the rights to the Curve codebase, which includes protection over the industry leading stableswap invariant which others have tried (and failed) to copy.

In fact, Curve considered pressing a copyright case against Saddle Finance for outright copying its code, but judged the returns from legal action against the fledgling protocol to be too minimal to justify the costs. Curve instead waited for the competitor to simply die out.

None have yet dared to replicate Curve’s more complex recent offerings, like the innovative liquidation protections of $crvUSD and the v2 formula with best in class automated liquidity optimization for trading volatile pairs. However, these proprietary algorithms have gained the attention of banks for cross-border settlement.

See: Project Mariana

Has it developed any network effects?

Setting aside the storied “Curve Wars,” let’s just look at internal network effects.

The launch of Curve v2 pools, which added trading of volatile assets in addition to the original competency for stablecoin trading, clearly produced network effects. From this point, every new pool that was launched through the permissionless factory and seeded grew Curve’s network effects — capturing more trading volume within Curve’s network.

Lately, the driver of network effects has been the interplay between Curve’s growing network of pools and its new and burgeoning $crvUSD business. The growth of $crvUSD is playing out across Curve’s network of v1 and v2 pools, to the delight of LPs…

What are it’s [sic] competitive advantage vs the field?

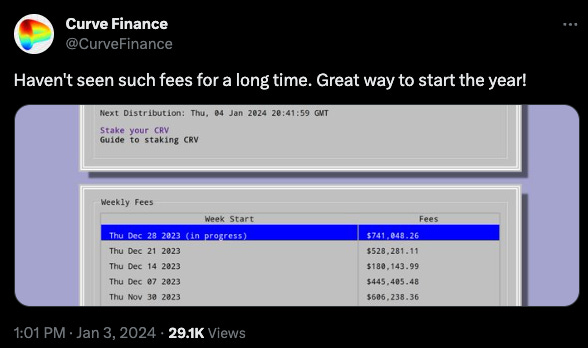

Curve consistently ranks in an elite tier in terms of revenue directed towards its userbase. This revenue is diversified and proving increasingly resistant to market downturns.

How good is the team in comparison with the field?

In all honesty, any serious observer could simply point to Curve’s deep entanglement with the bespoke devs of the Vyper ecosystem to answer this question.

But we don’t suspect most of Curve’s critics have the dev chops to recognize the subtleties of why this is such a game-changer, so we’ll just point to the popular reputation the team has cultivated on this subject.

How much skin in the game do they have?

The voracious complaining by haters about Mich’s proclivity to lend $CRV (instead of dumping it like other founders) could be reasonably rebranded as “golden handcuffs” if the haters possessed greater critical thinking skills. We’re not holding our breath.

How likely is it to grow?

Unlike investor-friendly memecoins, Curve revenue is now nicely diversified. Curve currently enjoys wonderful products to thrive whether the market is bearish (lending) or bullish (trading).

But we’re less interested in where we are, as much as where we’re going.

In particular, we’re bullish on the launch of isolated lending markets, which will bring something like a permissionless factory to the bespoke $crvUSD soft liquidation protections experience.

However, the industry writ large appears to be most bullish on new L2s, where Curve has shown a facility for establishing a toehold.

For more on the precambrian explosion of L2s, see the New Years prediction livestream from Leviathan