Sept. 26, 2022: Voter Guide 🗳️✅

Sept. 26, 2022: Voter Guide 🗳️✅

Votes on yCRV, CNC, Badger-FraxBP + Permissionless Reward Management

A spate of proposals hit the Curve governance forum over the past week. Here’s some notes to better inform your vote.

yCRV

The most contentious vote is the ongoing battle over Yearn’s yCRV.

There are two points of contention. The first is that the voting rights piece of the yCRV contract are unfinished, so users would be unable to cast an informed vote.

The second is some concerns around the vote locking mechanics. Vote locking is a mechanism to protect Curve against governance attacks, (see Beanstalk Finance). It also has the side benefit of aligning voters with the project in the longer term.

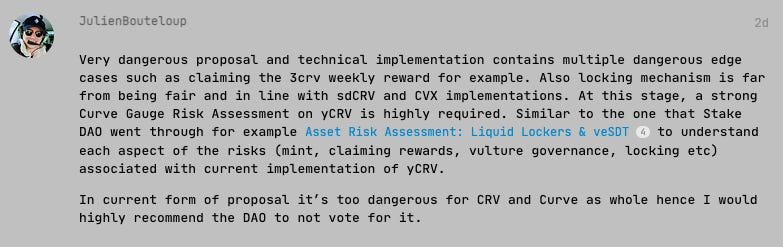

When protocols previously went through the governance process for their wrapped tokens, they also had lengthy community discussions about lock mechanisms. Julien Bouteloup of Stake DAO requested the mechanisms be in line with other wrapped versions of $CRV.

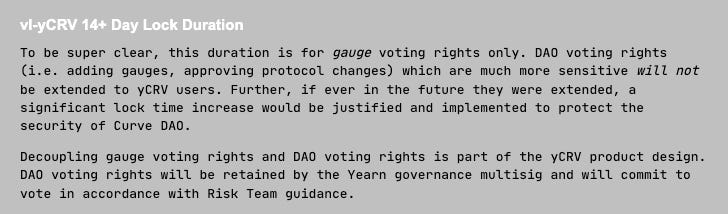

The mechanics of yCRV are intended to separate out the governance power for lower stake gauge votes with the higher stake votes for protocol changes. Wavey from Yearn described the mechanics in more depth:

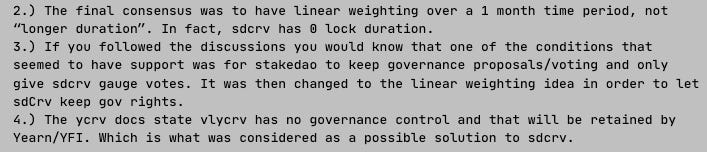

c2tp of Convex fame believes the conditions to be met

As for the urgency of acquiring a gauge before the contract is complete, Wavey added:

These are strong points, though we’d personally err on the side of waiting an extra week or so to allow for a thorough review by the Crypto Risks Team and others.

More on this from our article from last week:

CNC/ETH

Following our recommendation last week that users reject the CNC gauge vote for now, we were quite pleasantly surprised to see the Conic team chime in and agree.

So, that worked out better than expected. Relatively little to add, except to reiterate that we’re interested to see where this goes long-term.

Badger + FRAXBP

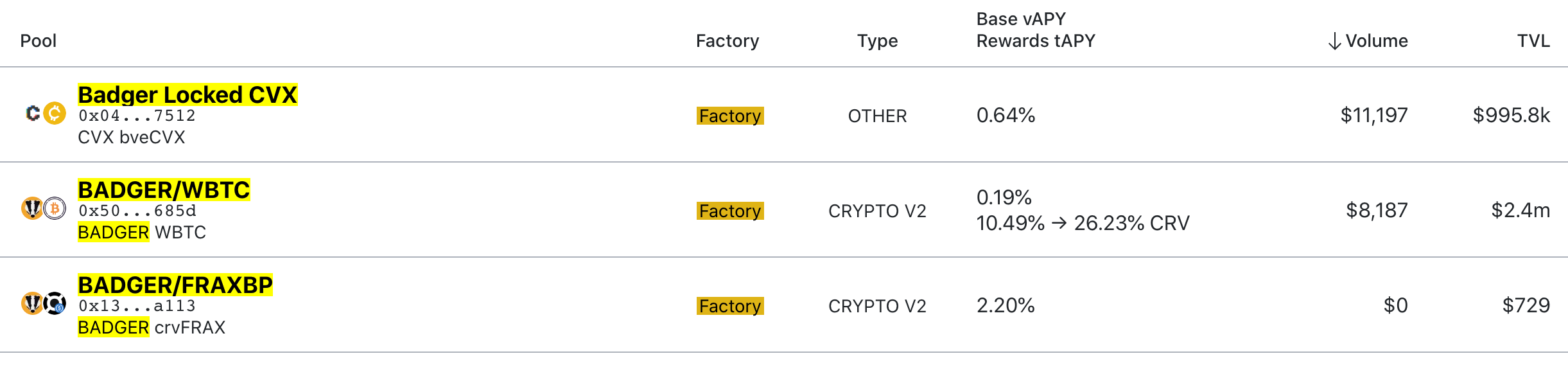

Another vote for a Badger / FraxBP pool has appeared. It appears to be uncontroversial, given that nobody has weighed in on the forum. On Convex, it has already passed quorum with over 13MM yes votes.

As the home of Bitcoin on Ethereum, Badger DAO is assembling an interesting ecosystem of Curve v2 pools.

The Badger / WBTC pool had been a great place to park wrapped Bitcoin, earning as high as 26% $CRV rewards. The risk here is impermanent loss, but this has lately been a non-factor, as the two tokens have largely traded in the same range recently. (OFC not financial advice, past performance not indicative of future returns, et al)

Opening a second v2 pool against Frax BP is a fun strategy. It’s quite common to pair ERC-20 tokens with $ETH, because at the end of the day most tokens on Ethereum tend to rise and fall with Etherum price. For an LP, such a pool may have less volatility, and therefore less impermanent loss as it trades like a stable pool.

When a crypto asset gets paired against a dollarcoin, the v2 pool gets more exposure to crypto volatility. In terms of trading fees, volatility is good for LPs. Curve 2 pools keep price parity specifically because arbitragers trade away the price difference after sudden movements. More volatility lead to more trades, which get returned to users in the form of fees.

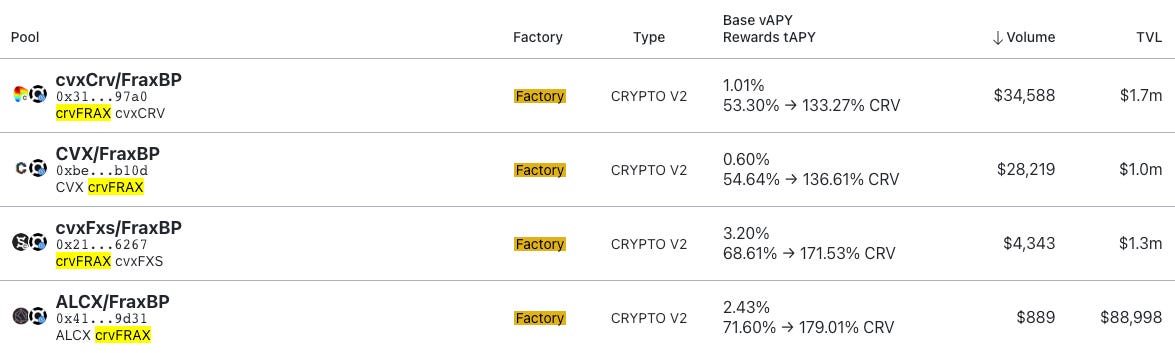

Sitting as an LP in the pool can be a bumpier ride, but the rewards are notable. Note the base vAPY:

Base vAPY on these pools is mostly north of 1%. The Curve v1 pools, which see trades due to user discretion as opposed to constant price re-arbitrages, tended to yield just a few basis points. Nobody paid much attention to trading fees in the v1 era. North of 1% real yields become more notable, (though below US treasury yields at the moment.)

You could be forgiven if you missed the vAPY for the more eye-popping rewards APY in the above screenshot. Any pool paired with FraxBP means heavy incentives. Here we outstrip treasury yields. Rewards tAPYs at an order of magnitude 100x the trading yields might outclass base vAPYs, but we know sky high rewards APYs are likely to fall, so it’s nice to have both.

The various FraxBP token paired pools are hidden gems here. Badger soon will be joining this list based on voting returns.

If you’re a trading type, you can even try to time these pools to buy / sell market trends (and earn rewards for the duration of time you’re in the position). Buy into the pool with the asset you think is overpriced, withdraw the asset you think is underpriced, just like bartering at your local market (NFA). Whenever you think crypto may pump, buy in with dollars and get hedged exposure plus good yields. See also…

Badger will soon have two well-incentivized pools where you can gain exposure to USDC or WBTC (similar to CVX vis a vis ETH) — meaning traders can flip their Badger stack into the pool corresponding with whichever direction they think the market is going.

If you think Badger is cheap, you buy into Badger-FraxBP with dollars and hope it goes up. If prices get high again some day, you can trade Badger to WBTC and cash out — or possibly park your Badger into the Badger / WBTC pool if you suspect Badger will fall first.

Upside or downside for guessing correctly, but in all scenarios where you’re in a Curve pool, you’re earning good yield, perhaps enough to paper over small price fluctuations. All in all, a smart play by Badger!

Permissionless Reward Management

This is an interesting one — thus far few people have cast a vote, perhaps waiting for more of an explanation.

The contract itself is rather simple, such that it would be comprehensible to a typical reader. It simply allows a designated user to add rewards to a Curve pool. Previously this typically ran through the DAO.

The argument in favor here would be that more rewards might flow through if there was reduced friction for protocols to add rewards. Once approved, a protocol may be more inclined to show LPs with a bonus if they don’t have to go through the lengthier slog of governance approval.

The counter-argument is that the current system is viable, whereas moving to a system where more people can do this permissionlessly just opens the door for error. Convex chad c2tp sounded a note of skepticism:

Skelletor rebuts this, pointing out it’s been working like this on most sidechains, and cites some specific examples on mainnet where it would have been useful.

We’re cautiously in favor of this, but also understand if the community feels it needs a bit more time to review the proposal.

Votes Past

cbETH

Uncontroversially sailing through governance was a vote for rewards on cbETH/ETH. Pay attention to this development. Coinbase’s $cbETH is a rather key part of the company’s broader strategy.

Pre-merge you hopefully were paying attention to our wrapped ETH one-pager, which highlighted that $cbETH was trading at a 6% discount to Ethereum (having been double digits prior). This has since closed to a 3% discount. Presuming nothing goes wrong, the intent is that $cbETH eventually becomes redeemable for 1 ETH plus staking rewards, so potential opportunity for long-term traders.

A gauge makes this more interesting, as users could park their cbETH in the pool and collect rewards in the meantime. Who would be interested in incentivizing this pool? Based on the white paper, we surmised Coinbase would not be interested in such tomfoolery.

Maybe this will turn out to be a bad prediction? Time will tell.

Votes Future

USDN Gauge Kill

Pay attention to this one. Following the Crypto Risks report on USDN, a governance forum request has been put through to kill the USDN rewards in an effort to drain liquidity from the pool. The team recommends migrating to a v2 pool which would be better equipped to handle the volatility.

See our prior article:

Links: Forum