Uptober 23, 2023: The $crvUSD Fee Switch 🎚️💸

"Maybe it's time indeed" to switch the fee token from 3CRV

Did you know that Curve is discussing a fee switch?

By “fee switch,” we are literally referring to switch-ing the token used for collecting Curve fees from $3CRV to $crvUSD

However unlike the “fee switch” being debated at other protocols, a Curve fee switch is actually likely to happen in our lifetimes. The limiting factor to the Curve fee switch is less the will of governance and more the technical chores needed to accomplish it.

“Maybe it’s time indeed” to make the move.

For some background, each week Curve prints a healthy amount of money in the form of fees. Half of this goes to stakers of veCRV. In the bull market, this tended to be millions of dollars, but in the bear market we’ve had to make do with a mere six figures.

Note: the amount of fees actually collected each week is presently undergoing a bit of a debate. We won’t get into the details of why this is so tough to calculate, but the short version is that so many small trickles of revenue from so many sources all get directed towards veCRV, making proper bookkeeping a bit tricky.

This complexity is a major reason that periodically some extra undiscovered money appears from an overlooked pool or chain, a phenomenon referred to occasionally as the ample Curve couch cushions…

July 6, 2023: The Cash Couch 🛋️💸

Thank you to all who turned out to ETH Barcelona and attended the panel on Risk Factors in Stablecoin/DeFi Design. Really enjoyed this conversation, make sure to follow giga-brain fellow panelists @TheBlockAdopter and @Tiza4ThePeople as well as the outstanding moderator

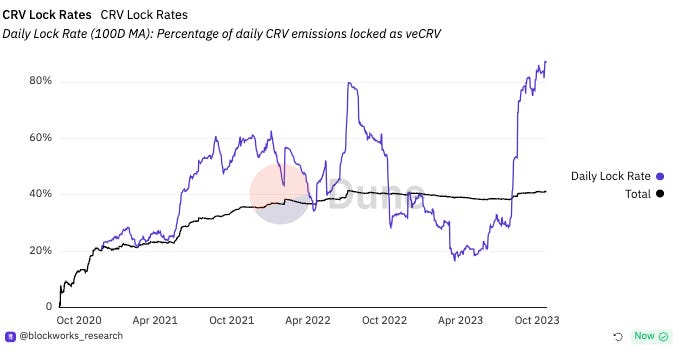

Whatever the actual amounts may be, perhaps the broader market is finally starting to glom onto the fact that Curve accrues and disburses steady and continuing cash flows. A rare example of cash flow in the waning days of a bera market may be what’s driving the elevated $CRV lock rate recently.

Each week a decent chunk of change gets collected and burned into $3CRV. The initiative now is to switch this from $3CRV to $crvUSD.

Why on earth would this matter? At the end of the day, you’re just getting a dollar out, right? Well, it turns out there’s more to it than that.

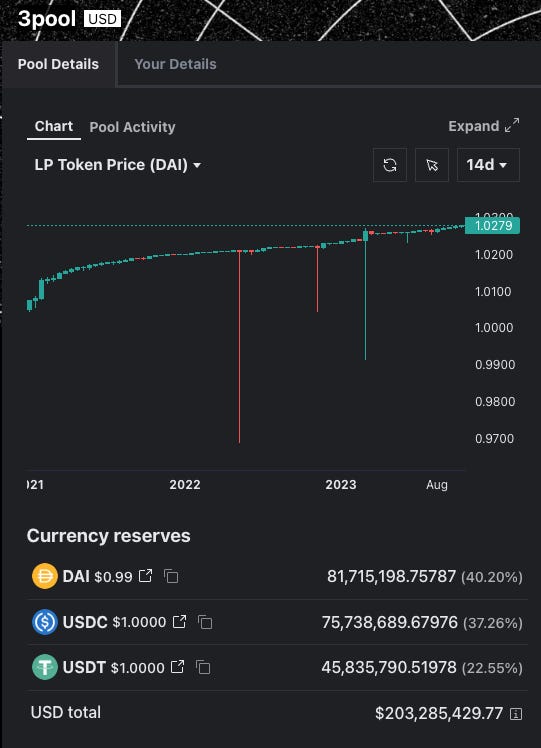

3CRV

Ah… good old trusty 3pool. Through all the wild swings of crypto, $3CRV has reliable.

One of Curve’s earliest pools. A pool that’s partly responsible for stablecoins ever gaining meaningful adoption. The ability to 24/7 safely trade meaningful volume between the two largest stablecoins at minimal cost helped the idea of stablecoins gain trust and usage in the first place.

The 3CRV LP token itself natively earned trading fees. These fees seldom exceed the yield one could get elsewhere in DeFi (or now, in non-Chase bank accounts). Yet the fact that it passively earned >0% and could be easily exited to three of the most important stablecoins in DeFi made it a comfy safe haven through the years.

More recently, the pool became so systemically useful it gained new life via “The Fiddy Indicator,” a trading tool used to guess if the ETH/BTC price was likely to dump or pump based on flows of Tether.

However, the era of $3CRV as a fee token may be winding to a close. It’s not so much that anything in particular is wrong with $3CRV. It’s more that switching to $crvUSD would more directly benefit the ecosystem.

$crvUSD

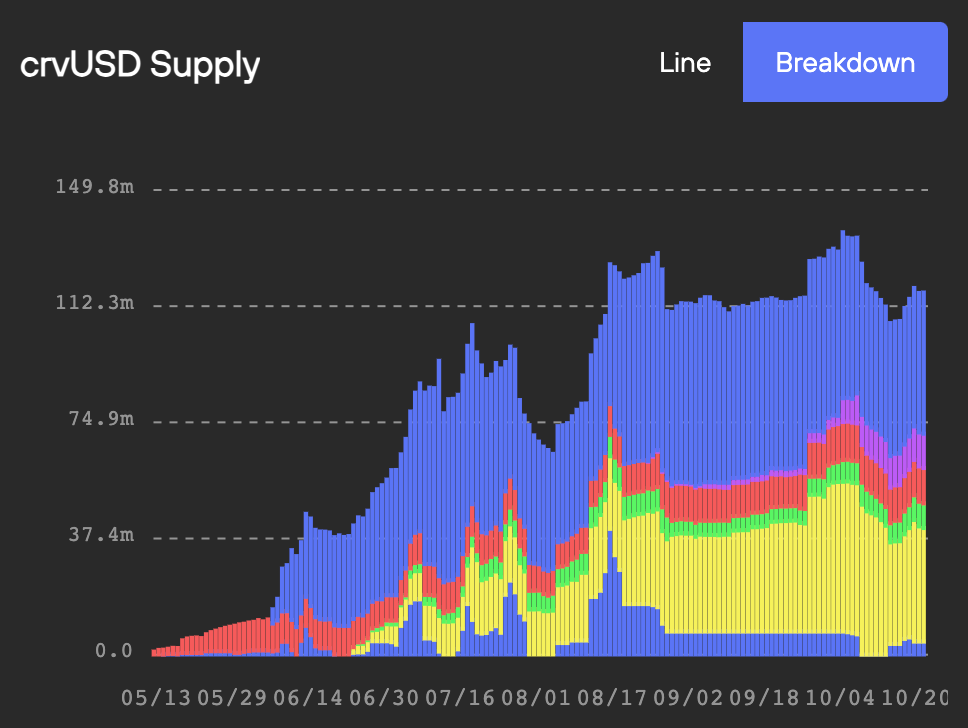

The successful launch of $crvUSD has ushered in a new era for Curve. Changing the fee token from $3CRV to $crvUSD can do a lot more to benefit the protocol at large.

In the way that new yield farms several years ago used to launch with $3CRV pairings, and then $FraxBP pairings, the locus of activity nowadays is the robust variety of trading pairs built against $crvUSD. It’s now a useful token in its own right, simply due to the variety of destinations and farms to which the token grants access.

More interestingly though, every $crvUSD in existence generates fees for Curve. The rate at which it prints varies wildly between 0-10%, but generally hovers around 5%

We’re at the point where Curve’s existence as a trading platform is seeing its revenue getting flippened by the revenue from ~$100MM $crvUSD in existence.

The impending launch of StableSwap-NG will allow for several more collateral types to get launched, helping fulfill dreams of hitting a $1 billion market cap for $crvUSD.

We’re entering into an era in which Curve revenue is well diversified, with a steady fees from $crvUSD even in boring markets, supplemented by periodic spikes from trading fees when volatility is high.

Most importantly, though, a move from $3CRV to $crvUSD as the fee token would reinforce the tokenomics of $crvUSD itself.

Every time Curve burns fees each week, it trades them onchain from whatever token into $3CRV. This creates constant demand for the token. However, demand for $3CRV only helps Curve as a protocol at the margins. If this was six to seven figures worth of buy pressure for $crvUSD instead, it could actually make a difference.

The $crvUSD that would get purchased by fee burners would get purchased from users who have minted $crvUSD at ~5% borrow rate and deposited to liquidity pools.

This borrow rate occasionally becomes a sore subject for borrowers. When rates spike too high, it becomes unprofitable and borrowers repay their loans en masse. High borrow rates may fuel good fees for the DAO, but the effects cancel out as $crvUSD growth stalls.

If only there was a way of keeping borrow rates lower.

The $crvUSD fee switch helps! Burning LP tokens to buy $crvUSD has the effect of reducing the amount of $crvUSD in the peg keeper pools. This drives the price of $crvUSD incrementally higher.

A higher price for $crvUSD means that the ecosystem tries to correct the imbalance by driving rates lower. Low rates cause Peg Keepers to take on debt by minting new $crvUSD, pushing supply higher.

The more liquidity sinks for $crvUSD, the more this effect plays out.

With $3CRV as fee token, we also saw a fair share of zombie liquidity. Users who earned a few dollars worth of $3CRV rewards might let it idle. It might cost too much in gas to yield farm or sell it. Strategically, it was best to just wait for a few more $3CRV fees to appear and transact later. Spread this effect over thousands of individuals, and you have a good chunk of $3CRV that exists and sensibly sitting stagnant.

As a fee token, a reservoir of stagnant $crvUSD would be printing money to the DAO. Every idle $crvUSD print money for the DAO because somebody is paying ~5% for the privilege of minting it. The more $crvUSD sprinkled broadly into wallets, the better.

In our view, creating more use cases for $crvUSD is the single action that most strongly benefits the broader Curve ecosystem. If you want to do anything to help pump $CRV, asking your favorite protocol to onboard $crvUSD is the step you can take today which will create the most bang for your stablecoin.

This is why we’ve seen a new “wen” has drop… “wen $crvUSD as fee token!!!!?!!11one”