July 27, 2022: Mythbusting🔬💥

Substantiating and Refuting Myths Around $CRV

Finding good info in the world of cryptocurrency is tough. Just as FUD-sters are keen to play up negative takes, maxis are equally keen to push positive info. Neither have incentive to carefully weigh the evidence.

Today we’re going to objectively scrutinize the evidence and data around popular narratives around $CRV. Admittedly, as a Curve maximalist, you would be wise to be skeptical of using me as a source. Yet I hope readers are persuaded by the quantity and data-driven nature of the evidence provided, the earnest attempt to fairly articulate both sides of the argument, and the generally fair conclusions (we do not resolve myths in only one direction) — please let me know if you object though!

If nothing else, the evidence collected can hopefully serve as a useful resource for both FUD-sters and maxis alike. We also commit to updating this article with other evidence provided by readers!

There’s loads of possible myths to consider, but for this article we focus on the following myths and related lemmas:

Curve is Primarily a Stablecoin Exchange

Curve will Death Spiral when Emissions Run Out

Curve Emissions Drive TVL

A Drop in $CRV Token Price Will Reduce TVLs

Curve P/E Ratio is Too High

Curve P/E is >100

Curve Emissions are Higher Than Revenue

Curve is Primarily a Stablecoin Exchange: BUSTED

Curve got its start as a stablecoin-to-stablecoin site, and has a great architecture for facilitating stablecoin-to-stablecoin transactions. The composability of pools via metapools and factory base pools renders it particularly potent.

Yet the question of whether Curve is primarily used for stablecoin transactions is no longer true. One can collect this information easily at the bottom of the traditional Curve homepage https://curve.fi/

This value fluctuates wildly depending on activity. We eyeball it closely, and for at least for the past week at least, Crypto Volume share has been >50% for several days running now.

Most of this is off the back of TriCrypto, which has gotten picked up by some exchange aggregators and is thus a very steady routing option for trades among the three largest crypto assets.

Much of the reason that TriCrypto is driving high volumes is that it carries a very large median transaction size. Curve provides very low slippage, which is highly attractive to whales. Before the DeFi crash, TriCrypto could host even larger trades.

Generally, Curve v2 pools have been found to be very efficient for trading, so we don’t see strong evidence that crypto transaction volume are likely to drop off anytime soon.

Admittedly, this has been a rather quiet week for crypto, so if unusual activity happens stablecoin volume could reverse and outpace crypto volume. It’s certainly possible that crypto volume and stablecoin volume will flippen each other back and forth… or that stablecoin volume may reclaim the throne for some time.

At present, though, the notion that Curve is primarily a “stablecoin exchange” is not supported by the facts, it a great site for stablecoins with even greater volume driven by its volatile asset trades.

MYTH: Curve is Primarily a Stablecoin Exchange

STATUS: Busted

Curve Will Death Spiral When Emissions Run Out: INCONCLUSIVE

We’ll quickly label this one inconclusive because it’s impossible to know. The last $CRV will be emitted after 357 years, so very few people except this article’s author are likely be around to know.

It’s essentially impossible to predict what will happen within 300 years, or even within 1 year, within the wild world of cryptocurrency, so anybody claiming to know for certain one way or the other is simply lying.

When considering at a “death spiral” possibility… we can certainly note that Curve’s operations change quite rapidly — Curve today looks very different from one or two years ago. Should a potential death spiral loom on the horizon at any point in the next three centuries, an option exists for active developers to recommend a solution to the DAO to course correct.

We’ll break from neutrality to assert that if Curve does not continue to adjust and innovate upon their current state of operations between now and 300+ years in the future, then we would agree that Curve would likely die, and deservedly so.

To look at one case, we can point to partial evidence that v2 pools would outlast even a nuclear apocalypse. We have an essentially perfect A/B test with the legacy tricrypto1 and its replacement tricrypto2. Both have the same composition are therefore perfectly substitutable products, but one receives gauge emissions and the other doesn’t. Unsurprisingly, 99.8% of TVL has located into TriCrypto2 over TriCrypto1.

Yet a small amount of liquidity remains in TriCrypto1, which remains a functional pool despite every other trend working against it. Its internal price oracle remains accurate. It tends to update prices in a timely fashion, because if it gets too far out of line it provides a small arb opportunity that gets quickly chewed up. This ensures constant trading pressure for the pool. The $500K in liquidity may find it preferable to enjoy the small fees from this volume than suffer the price impact of withdrawing.

This could be said to constitute the most extreme stress test for a Curve pool, where there’s a directly better alternative. We can infer from this that v2 pools are very difficult to kill. Even when there’s a clearly superior and perfectly substitutable product, the pool stubbornly continues to exist and function well a full year later.

People making the argument Curve is at risk of a death spiral will be more presuasive if they include a satisfactory explanation of how v2 pools would die off in such a death spiral. A death spiral wouldn’t even constitute such harsh conditions as above, as there would be no clearly superior alternative place to locate capital in such a scenario.

At any rate, on this narrow subject, we can’t yet issue a ruling.

MYTH: Curve Will Death Spiral When Emissions Run Out

STATUS: Inconclusive

We can look at two related claims to add more color to this debate:

Related Myth 1:

Curve Emissions Drive TVL: PROBABLY TRUE

If Curve emissions don’t drive TVL, then there’s zero risk of a death spiral, so we should explore this argument.

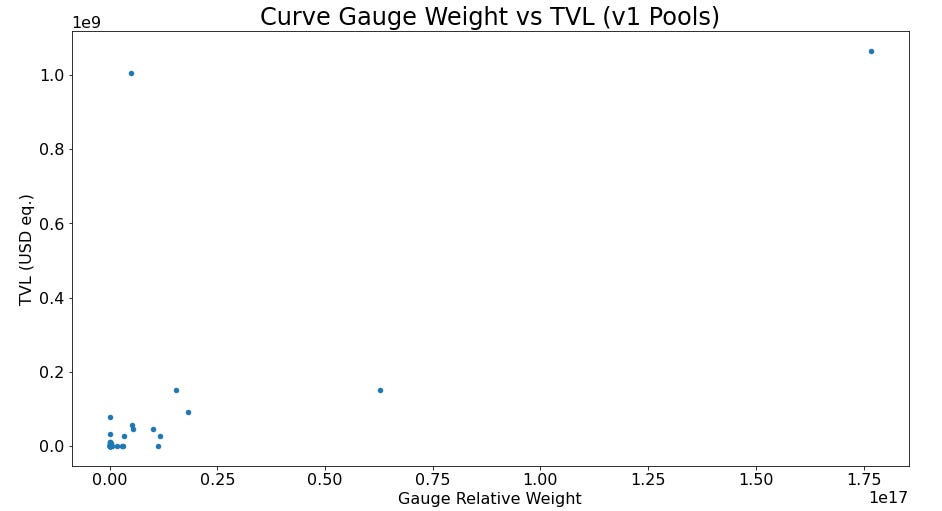

It appears to be true, at least for v1 pools. One can easily pull the pools relative gauge weights and the TVLs for v1 pools, which reveals about a 71% correlation.

Now this is a bit counterweighted by two outliers

Frax (upper right) carries a heavy gauge weight and a heavy TVL.

In the upper left is Curve 3pool, which has a very low gauge weight but tends to have high volume due to composability in other pools.

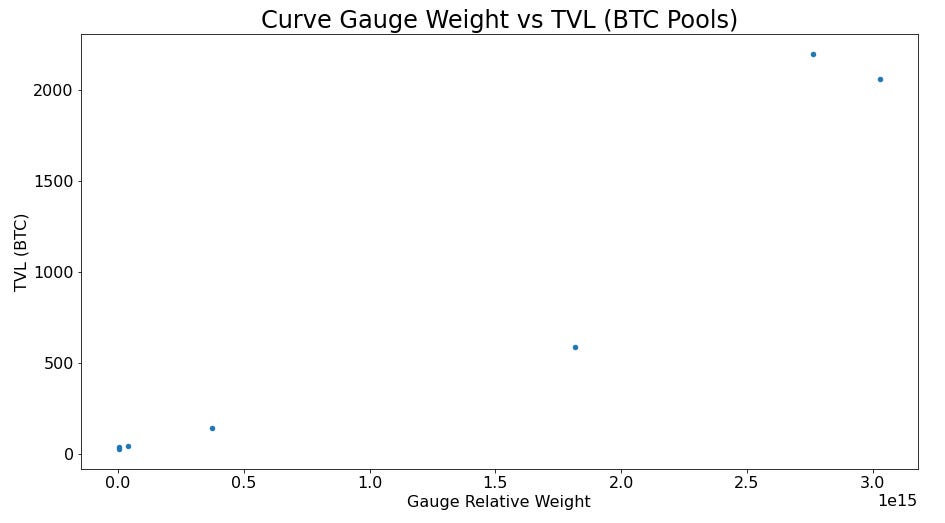

To get a sense of what this looks like for more ordinary v1 pools, you can prune this to just the BTC pools, which are a fairly representative slice given that they have occasional gauge weight rebalancing but fewer complicating factors. Here we see a direct 95% correlation between TVL and gauge emissions.

So the good news for protocols spending heavily to influence gauge weights, is that this appears to work, at least for v1 pools.

We excluded v2 pools simply because it was tougher for us to get a reasonable price data into our scripts, but glancing at the homepage suggests it’s a far more mixed bag.

Nowhere to be seen are the pools with the highest emissions, yet pools with relatively low emissions tend to creep into the list. Below this we even see v2 pools with no emissions doing reasonable business.

If we can see v1 pools as users having high elasticity due to several fairly substitutable pools within which to store their TVL, we might see v2 options as more distinct. So until we see more data on this subject, we can’t really opine. Hence we can only declare this true in part.

MYTH: Curve Emissions Drive TVL

STATUS: Probably True

RELATED MYTH 2:

A drop in the $CRV token price will reduce TVLs: PROBABLY FALSE

This is a common argument among $CRV skeptics. The narrative claims that a drop in Curve price should theoretically remove incentives to serve as a liquidity provider, and therefore would cause a reduction in TVL. This TVL reduction is what is meant to produce a negative feedback loop. Makes sense, right?

At the moment, advocates of this hypothesis have offered no supportive evidence beyond elegant thought experiments. We previously took a cursory glance at this and found the evidence did not substantiate the claim:

Another piece of evidence refuting the claim is that we’ve already recently seen examples of Curve behavior when $CRV emissions fell quite low.

However, we are not prepared to declare this completely debunked.

For one, advocates of this hypothesis deserve the opportunity to furnish evidence to bolster their claim. At this point we’d recommend their argument also take efforts to debunk these prior arguments in order to gain additional credibility.

More importantly, the evidence we’ve gathered against the claim is far from exhaustive. We’ve generally looked at windows in which the price of $CRV moved alongside the price of other cryptocurrency assets, but we did not isolate windows where the price of $CRV moved separately. One might argue that a drop in crypto prices across the board meant users had no relatively better options for LP-ing, whereas a drop in just $CRV could trigger such a flight.

However, given advocates of the hypothesis are yet unwilling or unable to offer a counterargument, we’re provisionally labeling this false based on the evidence provided to date.

MYTH: A drop in the $CRV token price will reduce TVLs

STATUS: PROBABLY FALSE

Curve P/E Ratio is Too High: INCONCLUSIVE

The argument has been advanced in various forms, notably by Arthur Hayes in dismissing Curve from consideration of potential DeFi investments.

Of course, the myth as worded is impossible to verify… “too high” is a value judgement. But under this umbrella we consider a spectrum of related statements that are easier to verify.

Curve P/E is >100: Probably False

Curve Emissions are Higher Than Revenue: True

What is Curve P/E? It’s extremely dependent on how one calculates this metric. P/E is straightforward to calculate for stocks, where you divide stock price per share by earnings per share.

For Curve in particular, it’s more complex. It depends on several factors, for which there’s no canonical answer:

Should Curve’s revenue include bribes or just trading fees

One would probably think all revenues should be included. Yet bribes are often not included, in part because they exist in several places and are tough to calculate. Further, a passive holder of veCRV may not collect bribes and see them expire.

What do you consider as total supply?

Given $CRV locking mechanisms, one might make a case for circulating supply, locked veCRV, total supply, or max supply, all of which are wildly different.

Circulating Supply refers to amount of $CRV out there, which makes some sense as it’s the amount of $CRV you could go find. Yet critics point out $CRV as a token technically earns 0, it must be locked to have any earning.

The argument for using Total Supply of veCRV (not shown in the above chart) is often advanced, because it is the ERC-20 token that actually has earnings. However, the token is not tradable, so does it technically have a price? You can make a good case it’s the same as the price of 1 $CRV, but this depends on duration of lock.

Total Supply as shown above considers total $CRV emitted to date. The argument here is that $CRV earns nothing, but could be locked and therefore has earnings potential. Detractors of this argue that some nonzero portion of veCRV will never be unlocked and should be removed from supply (in particular Convex locks, >50%)

Finally, one could use Max Supply to have a constant number. Yet max supply won’t be reached for over three hundred years, so it’s a bit misleading to consider supply that won’t hit the market for centuries.

So the use of P/E as a metric is essentially a value judgement. One can generate a higher or lower number depending on what numbers one selects.

It does seem clear that common P/E ratios quoted by TokenTerminal are definitively incorrect. Regardless of whatever formula they select, the revenue numbers are commonly rebutted. Curve trading volume, unlike bribes, is more straightforward to calculate correctly.

So the next point… Curve Emissions are higher than revenues. This is true.

We do know that Curve generates revenue. $100MM in trading fees for users, and $213MM in bribes. So we’ll use ~$300MM for total revenue generated.

We also know that Curve has released 1.7B $CRV token, about $2B worth, about 6.7x higher than total revenue generated. Objectively yes, this is higher.

What we’re not clear on is why it would be considered useful for this value to be lower. If Curve earned $300MM in revenue, and had only emitted, say, $100MM worth of tokens (for the sake of simplicity, let’s assume all revenue flows directly to holders of these tokens, no lock). Such a scenario would appear to simply indicate a severe mispricing. This token would be earning $3 in revenue and cost $1, so it’s free money that should be arbed up quickly. On this level, it seems fully natural for token emissions to necessarily be higher than revenues.

Of course the actual logic is different, but revenue generating tokens have a theoretical floor price of current revenues. On top of this, tokens carry a speculative premium which should at least be equal to the present value of all future revenues from existing and future revenue sources.

For $CRV, this might be thought to be the present value of all trading fees and bribes plus the chance of revenues from, say, $crvUSD or other products to be launched. For a token like $UNI it might be thought to be the present value of the weighted chance they turn on the fee switch plus governance value. Yet they should all carry some speculative premium.

Several commenters argue that token emissions should be counted as an expense. This constitutes a value judgement that also can’t be considered strictly true or false. Tallying this as an expense makes the accounting difficult for many cryptocurrency projects. Ergo the retort from Curve is to explicitly compare $CRV and $BTC tokenomics.

It’s a favorable comparison, given that Curve devs ship more than Bitcoin devs and have more revenue streams. Yet it wouldn’t satisfy a nocoiner arguing Bitcoin is also properly worth zero.

Until there’s a consensus, something like a generally accepted accounting principle for cryptocurrency, we have to consider this to be definitively inconclusive.

MYTH: Curve P/E Ratio is Too High

STATUS: INCONCLUSIVE

If you enjoyed this, let us know other myths to debunk! Or other evidence related to the myths we already reviewed! Disclaimers!